Price options and manage risk with our advanced Black-Scholes Greeks Calculator. Instantly compute call and put premiums, implied volatility, and exact values for Delta, Gamma, Theta, Vega, and Rho to optimize your trading strategies.

Black-Scholes Options Calculator

What exactly do the Black-Scholes Greeks measure in option pricing?

The Black-Scholes Greeks are mathematical risk measures derived from the Black-Scholes option pricing model. They quantify how sensitive an option's price (premium) is to specific changes in underlying market variables.

Essentially, they act as a risk-management dashboard for traders, allowing them to isolate and measure:

- Directional price changes

- Time decay

- Volatility shifts

- Interest rate fluctuations

By understanding these sensitivities, traders can hedge their portfolios against adverse market movements.

How does Delta indicate an option's directional risk and probability of expiring in the money?

Delta measures the expected dollar change in an option's price for a $1.00 movement in the underlying asset.

- Call options: Delta ranges from 0 to 1.

- Put options: Delta ranges from -1 to 0.

By defining how closely the option tracks the underlying asset, Delta reveals the position's directional risk. Furthermore, traders use Delta as a convenient proxy for the probability that an option will expire in-the-money (ITM). For example, a 0.30 Delta implies roughly a 30% chance that the option will finish ITM at expiration.

Why is Gamma crucial for understanding the rate of change and acceleration of Delta?

While Delta represents the "speed" at which an option's price changes, Gamma acts as the "acceleration." Gamma measures the rate of change in Delta for every $1.00 move in the underlying asset.

Gamma is crucial because Delta is not static; it constantly shifts as the stock price fluctuates. A high Gamma indicates that Delta can change violently with small underlying price movements, exposing traders to rapidly shifting directional risk. Monitoring Gamma helps traders anticipate how quickly their Delta exposure will expand or contract, which is especially critical for options near expiration.

How does Theta quantify the daily impact of time decay on an option's premium?

Theta represents the rate at which an option loses its extrinsic value as time passes, assuming all other market variables remain constant. It quantifies "time decay" by estimating the dollar amount the option's premium will decrease each day.

- Negative Impact: Theta is generally a negative number for option buyers because time is an enemy; the option loses value every day it isn't exercised.

- Acceleration: Time decay is not linear. Theta accelerates (becomes increasingly negative) as the expiration date approaches, punishing at-the-money options the most during the final weeks of their lifecycle.

Why does Vega measure price sensitivity to changes in implied volatility rather than historical volatility?

Vega measures an option's price sensitivity to a 1% change in implied volatility (IV). It focuses on implied rather than historical volatility because the Black-Scholes model is strictly forward-looking.

Historical volatility merely reflects past price fluctuations, which cannot accurately predict future uncertainty. Implied volatility, however, represents the market's current expectation of future price movement over the option's remaining lifespan. Because options are priced based on the probability of future payoffs, Vega must rely on forward-looking IV to correctly gauge the premium associated with future market turbulence.

How does Rho reflect the impact of risk-free interest rate fluctuations on option values?

Rho measures the expected change in an option's price for a 1% change in the risk-free interest rate (typically based on U.S. Treasury bills).

- Call Options: Have a positive Rho. Higher interest rates increase call premiums because buying calls requires less capital than buying the stock outright, allowing traders to earn interest on the saved cash.

- Put Options: Have a negative Rho. Higher rates decrease put premiums due to the delayed potential cash received from shorting the underlying asset.

Rho is generally the least scrutinized Greek, but it becomes vital in high-rate environments or for long-dated options (LEAPS).

How do traders actively use these metrics to construct delta-neutral hedging strategies?

Traders construct delta-neutral portfolios by balancing positive and negative Delta positions so the net Delta equals zero. This mathematically insulates the portfolio from small directional price movements.

- Assess current Delta: Calculate the total combined Delta of all options and stock in the portfolio.

- Offset the risk: Buy or sell the underlying asset (or other options) to neutralize the total. For example, to hedge a portfolio with a +500 Delta, a trader will short 500 shares of the underlying stock (Delta = -500).

- Dynamic Hedging: Because Gamma constantly alters Delta, traders must continuously buy or sell shares to rebalance and maintain the zero-Delta state.

In what ways do the individual Greeks shift as an option moves from out-of-the-money to in-the-money?

As an option's moneyness transitions, the Greeks undergo significant behavioral shifts:

| Greek | Out-of-the-Money (OTM) | At-the-Money (ATM) | In-the-Money (ITM) |

|---|---|---|---|

| Delta | Approaches 0 | Near 0.50 (or -0.50) | Approaches 1.0 (or -1.0) |

| Gamma | Low | Highest (Peaks) | Low |

| Theta | Low decay | Maximum daily decay | Low decay |

| Vega | Low sensitivity | Maximum sensitivity | Low sensitivity |

How does the time remaining until expiration specifically alter the behavior and magnitude of Gamma and Vega?

Time to expiration has a profound, inverse effect on the magnitudes of Gamma and Vega:

- Gamma: As expiration approaches, Gamma explodes for at-the-money (ATM) options. With very little time left, the Delta of an ATM option becomes hyper-sensitive, violently snapping between 0 and 1 with tiny stock movements.

- Vega: Conversely, Vega drops for all options as expiration nears. Options with more time until expiration have much higher Vega because there is ample time for future volatility to impact the stock. Short-term options are practically unaffected by broad changes in implied volatility.

What are the primary limitations and theoretical assumptions of relying on Black-Scholes Greeks in real-world trading?

Relying purely on Black-Scholes Greeks introduces risk due to the model's rigid theoretical assumptions:

- Constant Volatility: The model assumes volatility remains perfectly constant, completely ignoring real-world volatility smiles, skew, and sudden spikes.

- European Constraints: It is designed for European options (exercisable only at expiration), making it mathematically imprecise for American options which allow early exercise.

- Normal Distribution: It assumes asset returns are log-normally distributed, which severely underestimates the frequency and impact of extreme market crashes (fat tails).

- Frictionless Markets: It assumes continuous trading, perfect liquidity, and zero transaction costs, which fail during market gaps or trading halts.

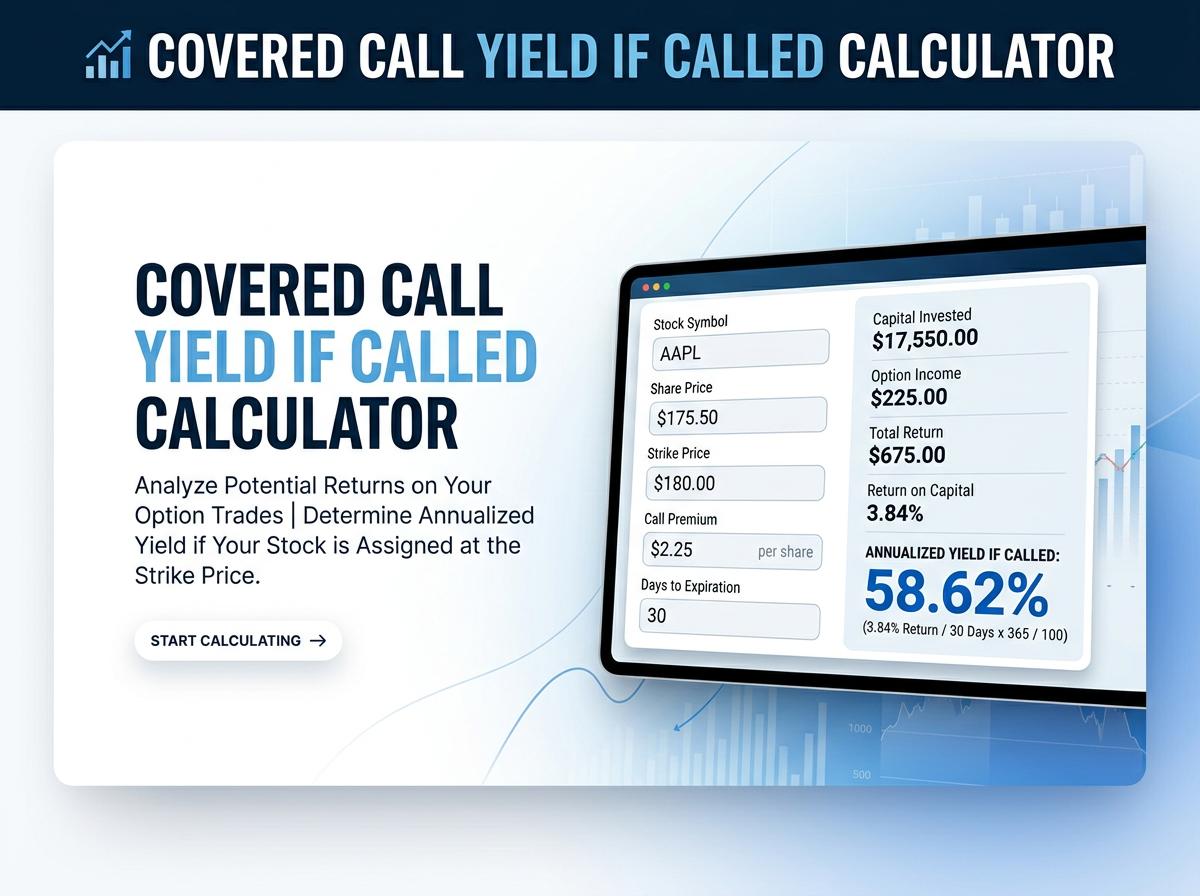

Covered Call Yield if Called Calculator

Covered Call Yield if Called Calculator