Browse Calculators

What inputs are required to use an auto finance calculator accurately?

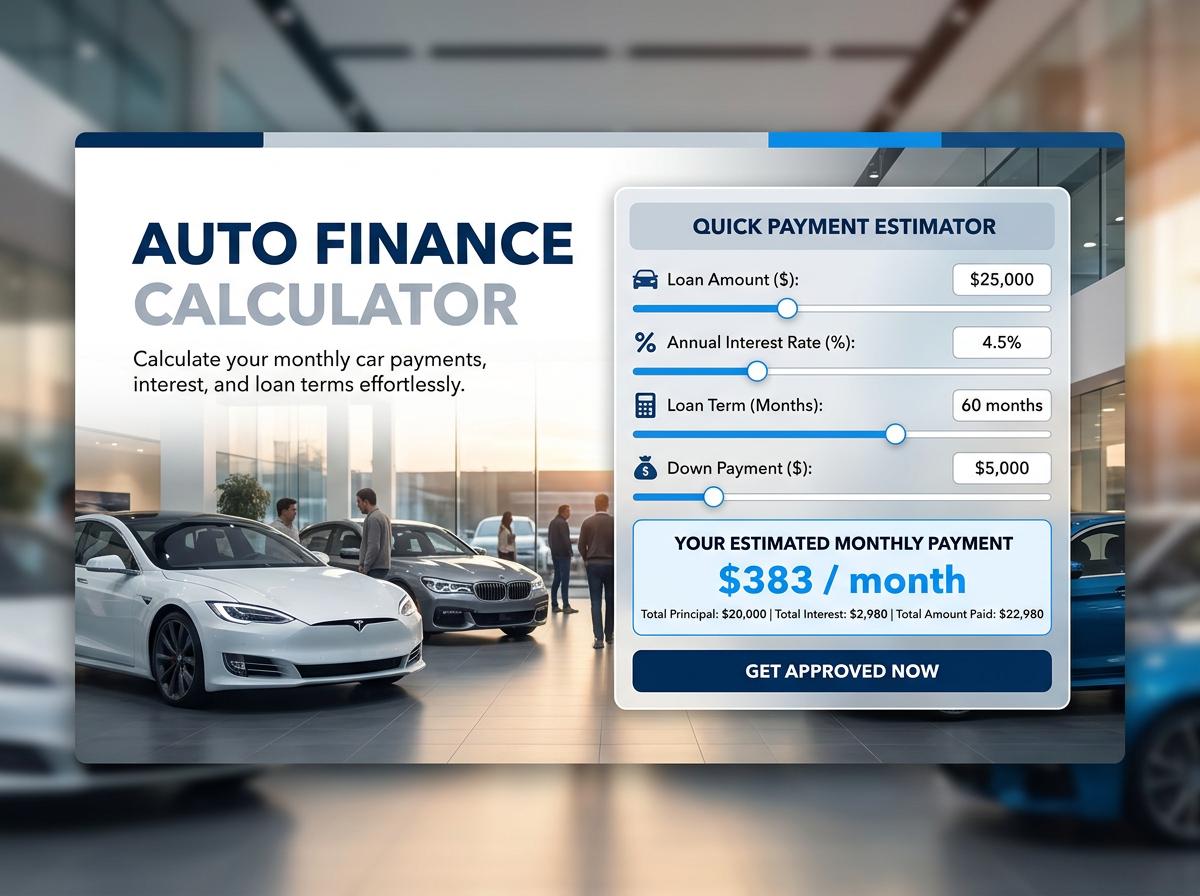

To get the most accurate estimate from an auto finance calculator, you typically need to provide the following key inputs:

- Vehicle Price: The negotiated purchase price of the car.

- Down Payment: The amount of cash you plan to pay upfront.

- Trade-in Value: The estimated value of your current vehicle, minus any remaining loan balance.

- Loan Term: The duration of the loan, usually expressed in months (e.g., 36, 48, 60, or 72 months).

- Interest Rate (APR): The expected annual percentage rate based on your credit score.

- Sales Tax Rate: Your local state and city sales tax percentage.

How does the length of the loan term affect the monthly payment?

The length of your loan term has a direct and opposing impact on your monthly payments and the total interest paid.

| Loan Term | Monthly Payment | Total Interest Paid |

|---|---|---|

| Shorter (e.g., 36 months) | Higher | Lower |

| Longer (e.g., 72 months) | Lower | Higher |

While stretching a loan over 72 or 84 months makes the monthly payment more affordable, it keeps you in debt longer. Because interest accrues over a longer period, you will ultimately pay significantly more for the vehicle overall.

Can the calculator factor in the value of a vehicle trade-in?

Yes, most comprehensive auto finance calculators allow you to input the value of a trade-in vehicle. The trade-in value acts exactly like a cash down payment—it reduces the total capitalized cost of your new vehicle.

When you enter a trade-in amount, the calculator subtracts this value from the purchase price before applying the interest rate. If you still owe money on your trade-in (negative equity), some advanced calculators allow you to input the remaining loan balance. The calculator will then add that negative equity to the new loan amount, accurately reflecting your new monthly payment.

Does the estimated payment include sales tax and local dealership fees?

It depends entirely on the specific calculator you use. Basic calculators only calculate principal and interest based on the vehicle price, ignoring taxes and fees. This can result in a deceptively low monthly payment.

More advanced calculators include specific fields for:

- Sales Tax: Calculates tax on the purchase price (or the difference between the price and trade-in, depending on state laws).

- Dealership Fees: Documentation and processing fees.

- Title and Registration: State DMV fees.

If a calculator lacks these fields, you should manually add 7% to 10% to the vehicle's purchase price to account for these extra costs.

How does changing the down payment alter the total cost of the loan?

Changing your down payment significantly alters both your monthly obligation and the overall cost of the loan. When you increase your down payment, you achieve two primary benefits:

- Lower Principal: You are borrowing less money from the lender.

- Reduced Interest: Because interest is calculated as a percentage of your principal balance, borrowing less means less money accrues interest over the life of the loan.

Consequently, a higher down payment lowers your monthly payment and decreases the total cost of the loan. Conversely, making a small down payment maximizes the principal, resulting in higher monthly payments and substantially more interest paid over the years.

What is the difference between interest rate and APR in the calculation?

While often used interchangeably, interest rate and APR (Annual Percentage Rate) represent two different metrics in auto financing.

| Metric | Definition | What it Includes |

|---|---|---|

| Interest Rate | The basic cost of borrowing the principal loan amount. | Just the baseline percentage charged by the lender. |

| APR | The true, total yearly cost of borrowing money. | Interest rate plus lender fees, origination fees, and prepaid finance charges. |

For accurate calculations, you should always use the APR, as it provides a complete picture of your actual borrowing costs.

Will the calculator show the total amount of interest paid over time?

Yes, any quality auto finance calculator will clearly display the total amount of interest paid over the life of the loan. This is one of the most critical figures to review, as it shows the true cost of financing the vehicle.

Many calculators provide a detailed amortization schedule. This is a table or graph breaking down every single monthly payment from the start to the end of the loan. It illustrates exactly how much of each payment goes toward the principal balance versus the interest charges, showing how the interest portion shrinks over time.

How reliable are the calculator results compared to actual lender offers?

Calculator results are mathematically perfect based on the numbers you input, but they are only estimates compared to actual lender offers. Their reliability depends heavily on how realistic your inputs are.

The biggest variable is the APR. A calculator lets you input any rate you want, but an actual lender determines your rate based on your credit score, credit history, vehicle age, and current market conditions. Additionally, lenders may calculate interest slightly differently or include mandatory fees that you didn't account for in the online tool. Always treat calculator outputs as a baseline guide.

Does using an online car loan calculator impact my credit score?

No, using an online car loan calculator has absolutely no impact on your credit score. Auto finance calculators are purely mathematical tools that operate locally on your web browser or via an anonymous server request.

They do not ask for your Social Security Number, and they do not communicate with credit bureaus like Experian, Equifax, or TransUnion. Because there is no "hard inquiry" or "soft inquiry" pulled against your credit profile, you can use these calculators as many times as you want to run different financing scenarios safely.

Can the tool be used to estimate payments for leased vehicles?

Generally, no. A standard auto loan calculator uses simple amortization (paying off the entire principal plus interest over time). Leasing requires a completely different mathematical formula.

To calculate a lease, you need a dedicated Auto Lease Calculator that factors in:

- Capitalized Cost: The negotiated price of the car.

- Residual Value: The estimated value of the car at the end of the lease.

- Money Factor: The lease version of an interest rate.

Because lease payments only cover the vehicle's depreciation during the term, plugging lease numbers into a standard loan calculator will yield inaccurate results.