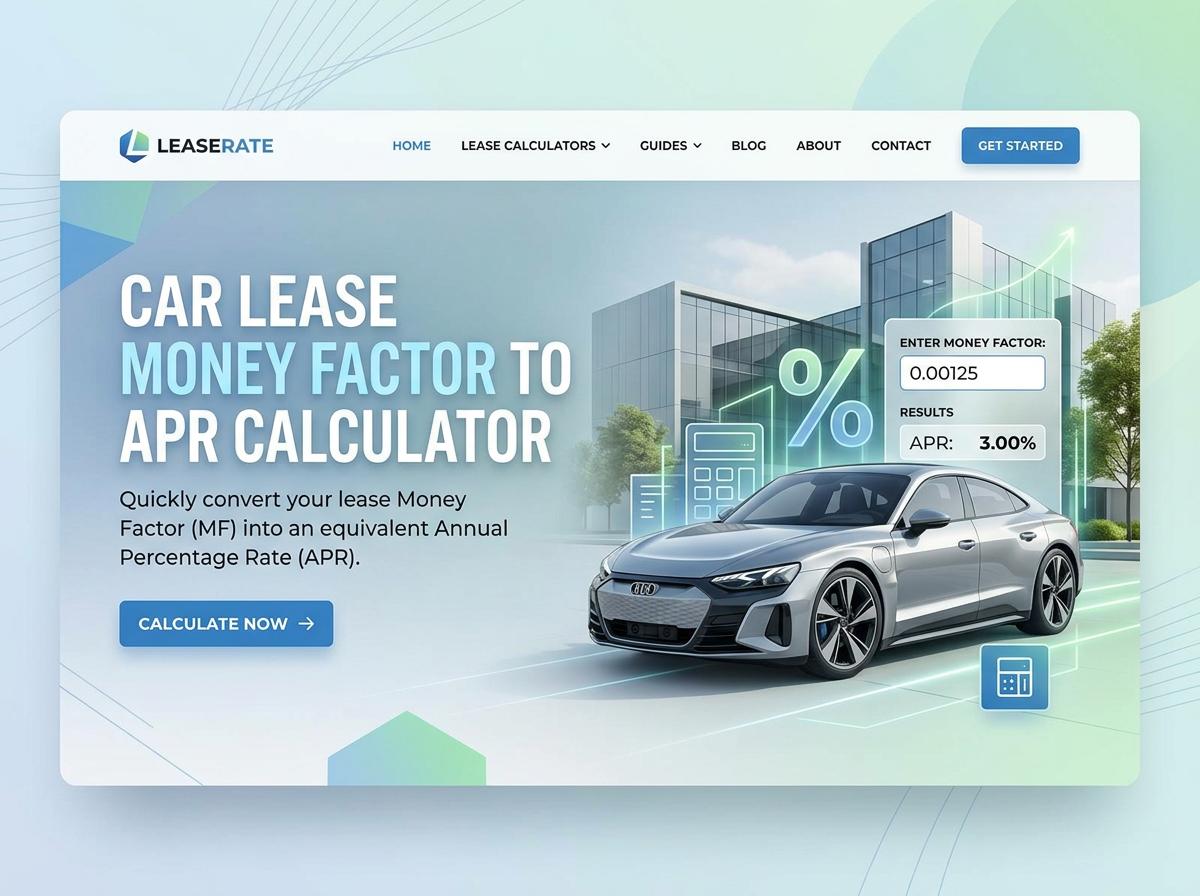

Instantly convert your car lease money factor to APR with our free online calculator. Uncover your true lease interest rate, compare auto financing deals, and negotiate better terms in seconds.

Lease Money Factor Calculator

What exactly is a car lease money factor?

A car lease money factor (also known as a lease factor or lease fee) is a method used by dealerships and lenders to determine the financing charge on a leased vehicle. Essentially, it represents the interest rate you pay to borrow the car's value during the lease term.

Instead of being expressed as a standard Annual Percentage Rate (APR), it is shown as a small decimal number, usually preceded by several zeros (e.g., 0.00125). The money factor is multiplied by the sum of the vehicle's capitalized cost and its residual value to calculate your monthly finance fee.

How do you convert a lease money factor to an APR?

Converting a lease money factor to an Annual Percentage Rate (APR) is straightforward. You simply multiply the money factor by 2,400.

- Formula: Money Factor × 2,400 = APR Percentage

- Example: 0.00150 × 2,400 = 3.6% APR

Conversely, if you know the APR and want to find the equivalent money factor, you divide the APR by 2,400 (e.g., 4.8% ÷ 2,400 = 0.00200). This simple mathematical trick helps consumers understand complex lease financing charges in the more familiar terms of standard auto loan interest rates.

Why is the money factor multiplied by 2400 to get the interest rate?

The number 2,400 is not arbitrary; it is a mathematical shortcut derived from the formula used to calculate the average monthly interest over a lease. Here is the breakdown:

- The standard finance formula calculates interest based on the average amount financed: (Capitalized Cost + Residual Value) ÷ 2.

- To get a monthly rate from an annual rate (APR), you divide the APR by 12 months.

- Since APR is a percentage, converting it to a decimal requires dividing by 100.

Combining these denominators gives you the magic number: 2 (for the average) × 12 (months) × 100 (percentage) = 2,400. Multiplying the money factor by 2,400 simply reverses this equation.

What is considered a good money factor for a standard lease?

A "good" money factor fluctuates based on current market interest rates, federal reserve rates, and the lessee's credit profile. Generally, you want a money factor that converts to an APR comparable to or lower than average new car loan rates.

| Money Factor | Estimated APR | Rating |

|---|---|---|

| 0.00000 - 0.00083 | 0% - 2.0% | Excellent (Often Subsidized) |

| 0.00084 - 0.00166 | 2.0% - 4.0% | Good |

| 0.00167 - 0.00250 | 4.0% - 6.0% | Average |

| 0.00251+ | 6.0%+ | Poor to High |

How heavily does the money factor impact your monthly payment?

The money factor heavily impacts your monthly lease payment because it dictates your total finance charge. A lease payment consists of three main parts: vehicle depreciation, taxes, and the finance charge (rent charge).

If you agree to a high money factor, a substantial portion of your monthly payment will go toward interest rather than paying down the vehicle's depreciation. For example, on a $40,000 leased vehicle, a money factor of 0.00300 (7.2% APR) could result in finance charges exceeding $150 per month. Lowering that money factor to 0.00125 (3.0% APR) cuts the monthly finance charge by more than half, directly reducing your overall monthly payment.

Are money factors negotiable with the dealership?

Yes, the money factor is often negotiable, but with some strict limitations. Lenders set a "buy rate," which is the minimum base money factor you qualify for based on your credit score. The dealership cannot negotiate below this buy rate.

However, dealers are legally allowed to mark up the buy rate to increase their profit margin. If a dealer presents a marked-up money factor, you can absolutely negotiate it down. To do this effectively, research the manufacturer's current base buy rate on leasing forums beforehand and demand that the dealership matches it.

Are dealers legally required to disclose the money factor to you?

Surprisingly, no. Under the federal Consumer Leasing Act (Regulation M), dealerships are required to disclose many elements of a lease contract, including the capitalized cost, residual value, total monthly payment, and the total finance charge (rent charge).

However, they are not legally mandated to disclose the specific money factor used to calculate those charges. Because it is rarely listed directly on the standard lease contract, consumers must proactively ask the finance manager for the exact money factor. If the dealer refuses to disclose it, you can calculate it yourself using the total rent charge.

How does your credit score affect the money factor you qualify for?

Your credit score is the primary determinant of the base money factor (buy rate) a lender will offer you. Lenders use credit tiers to evaluate risk:

- Tier 1 (Excellent Credit, 720+): Qualifies for the lowest base money factors and exclusive promotional lease specials.

- Tier 2 (Good Credit, 680-719): Receives average money factors with a slight bump in interest compared to Tier 1.

- Tier 3 & Below (Fair/Poor Credit, <680): Assigned significantly higher money factors to offset the lender's risk of default.

Ultimately, a lower credit score translates to a higher money factor, making the lease much more expensive.

Can a dealership mark up the base money factor provided by the lender?

Yes, dealerships frequently mark up the base money factor provided by the lender. The lender issues a base rate (the "buy rate") depending on the customer's credit profile. Dealerships are then permitted to inflate this rate (creating the "sell rate") before presenting it to the customer.

The difference between the buy rate and the sell rate generates a hidden profit known as the "reserve" or "dealer markup." The lender then splits this extra profit with the dealership as a commission for originating the loan. Knowing your credit score and researching the base rate helps prevent this.

How does knowing the APR help you compare leasing versus buying?

Converting the lease money factor to an APR allows for a direct, apples-to-apples comparison between the cost of leasing and the cost of buying a vehicle with a traditional auto loan. Since auto loans are universally advertised using APR, the tiny decimal format of a money factor obscures the true borrowing cost.

By doing the "multiply by 2,400" calculation, you might discover that a seemingly attractive lease actually carries an equivalent APR of 8%, while a traditional purchase loan might offer a 4% APR. This transparency empowers you to choose the most cost-effective financing route.

Sources:

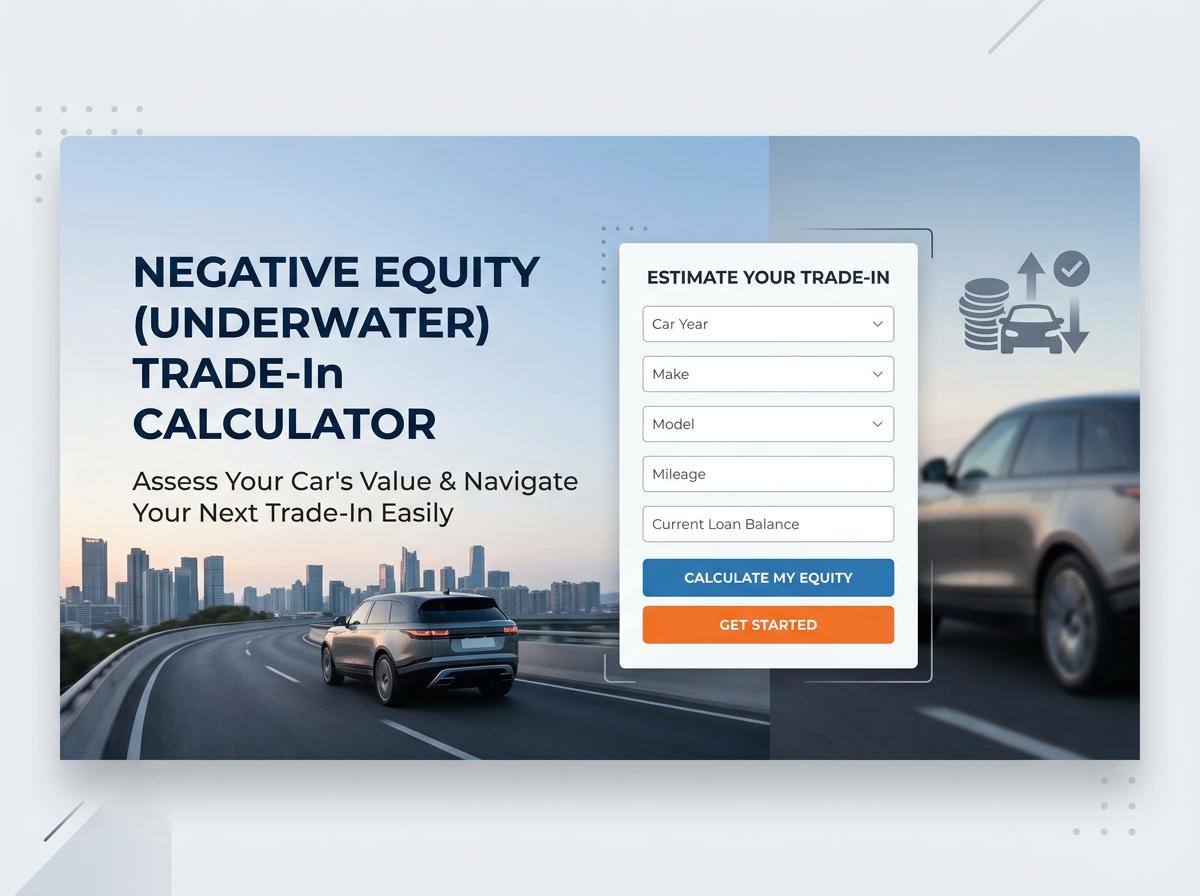

Negative Equity (Underwater) Trade-In Calculator

Negative Equity (Underwater) Trade-In Calculator