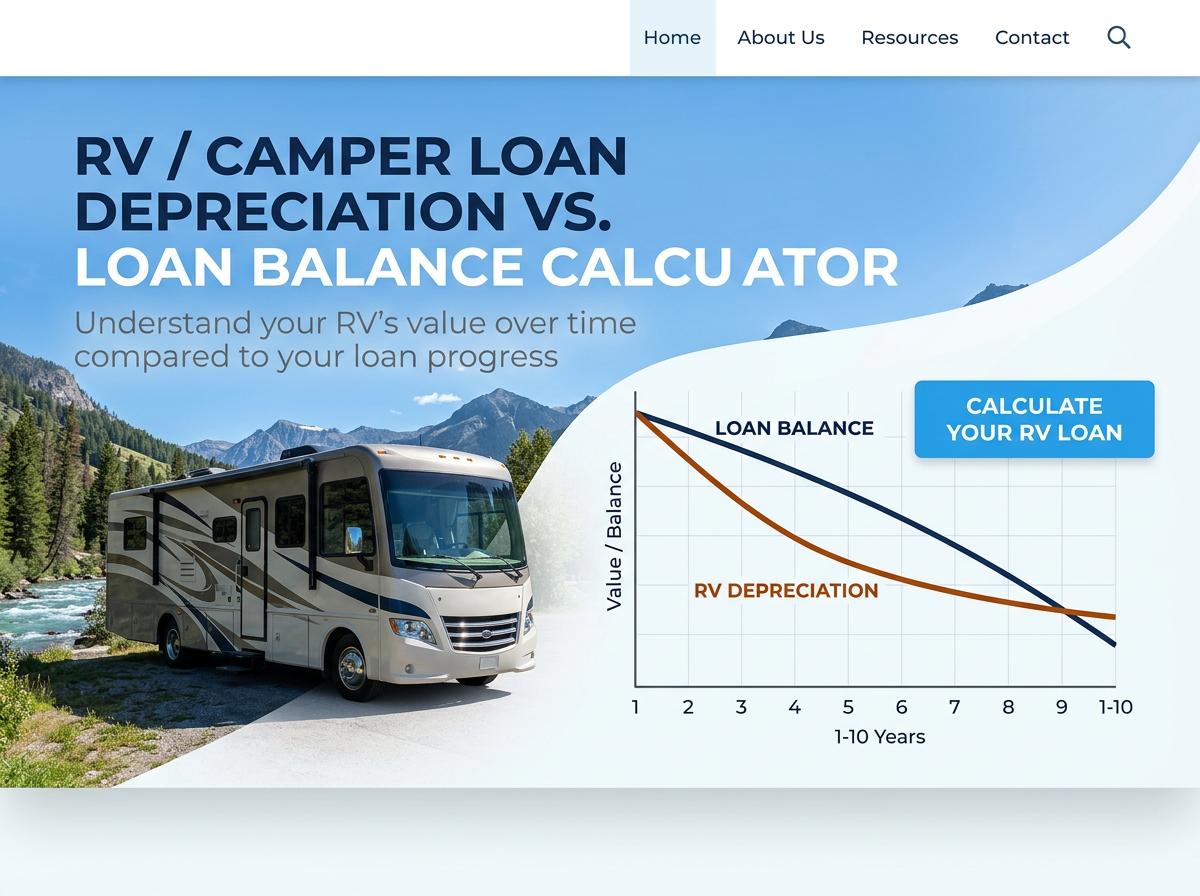

Find out if you are upside down on your RV loan. Use our free RV and Camper Loan Depreciation vs. Loan Balance Calculator to compare your vehicle's projected value against your remaining payoff amount. Track negative equity, plan your payoff strategy, and make smarter financial decisions when buying or selling.

RV Depreciation vs. Loan Calculator

How quickly does a new RV lose its value in the first few years compared to a standard car?

A new RV generally depreciates faster and more severely than a standard passenger car, especially in the first few years. While a new car loses about 20% of its value in the first year, a new RV can lose up to 30% the moment it leaves the dealership lot.

| Timeframe | Average RV Depreciation | Average Car Depreciation |

|---|---|---|

| End of Year 1 | 20% - 30% | ~20% |

| End of Year 3 | 30% - 40% | ~30% |

| End of Year 5 | 40% - 50% | ~40% |

Motorhomes (Class A, B, C) typically hold value slightly better than towable travel trailers, but both depreciate substantially faster than daily-driven automobiles.

What does it actually mean to be upside down or underwater on an RV loan?

Being "upside down" or "underwater" on an RV loan is a financial situation known as negative equity. It means that the current outstanding balance of your loan is higher than the actual market resale value of the camper.

For example, if you owe $45,000 on your RV loan, but the fair market trade-in value of the RV has dropped to $35,000, you are upside down by $10,000.

- Consequence: You cannot simply sell or trade in the RV to clear the debt.

- Risk: If the RV is totaled, insurance will only pay the $35,000 value, leaving you responsible for the remaining $10,000.

How do long-term RV loans increase the risk of owing more than the camper is currently worth?

RV loans often span 10 to 20 years to keep monthly payments affordable on large purchase prices. This long-term structure creates a severe risk of negative equity due to two clashing factors:

- Rapid Depreciation: The RV loses a massive chunk of its value in the first five years.

- Slow Principal Reduction: Long-term loans use an amortization schedule that heavily front-loads interest. During the first few years, the majority of your monthly payment goes toward bank interest, not reducing the actual loan balance.

Because the RV's value falls rapidly while the loan balance barely decreases, a widening gap forms, leaving the owner significantly underwater for a decade or more.

Is gap insurance necessary to cover the financial difference if the RV is totaled or stolen?

Yes, gap (Guaranteed Asset Protection) insurance is highly recommended and often considered necessary if you finance a new RV with a low down payment or a long loan term.

Standard RV insurance policies only pay out the Actual Cash Value (ACV) of the vehicle at the time of the loss. Because of rapid depreciation, the ACV is frequently much lower than your loan balance. Gap insurance steps in to pay the "gap" between the depreciated value of the totaled RV and the amount you still owe the lender, saving you from paying thousands of dollars out-of-pocket for a camper you no longer possess.

How does making a substantial down payment help protect against negative equity?

Making a substantial down payment (typically 20% or more) acts as a protective financial buffer against the steep initial depreciation of a new RV.

When you put zero money down, your loan balance starts at 100% of the RV's retail price (plus taxes and fees). As the RV instantly loses 20% of its value driving off the lot, you are immediately underwater. By making a 20% down payment, your starting loan balance is already reduced to match the depreciated value of the camper. This keeps you at a "break-even" point, ensuring that your loan balance stays relatively aligned with the RV's resale value over time.

What are my options for selling my camper if the loan balance is higher than its resale value?

Selling an underwater RV is difficult because the lender will not release the title until the loan is fully satisfied. Your main options include:

- Pay the Difference Out-of-Pocket: Sell the RV for market value and use your own cash savings to pay the lender the remaining negative balance.

- Take Out a Personal Loan: If you lack cash, you can acquire an unsecured personal loan to cover the negative equity gap, allowing you to transfer the title to the buyer.

- Private Sale: Try to sell the RV privately rather than trading it in. Private party sales generally yield higher prices than dealership trade-in values, minimizing the negative equity gap.

Does buying a used RV significantly reduce the gap between loan amortization and depreciation?

Yes, buying a gently used RV (typically 2 to 5 years old) is one of the best ways to avoid negative equity. By purchasing used, you allow the original owner to absorb the steepest, most punishing period of depreciation.

Because the used RV has already experienced its largest value drop, its future depreciation curve is much flatter. Consequently, even with an amortized loan, your monthly principal payments are much more likely to keep pace with the slower rate of depreciation, drastically reducing the risk of ending up upside down on the loan.

How does the structure of loan amortization affect how much principal is paid off early on?

Amortized loans are structured so your total monthly payment remains fixed, but the internal ratio of interest to principal shifts over the life of the loan.

Lenders front-load the interest calculations based on the total remaining balance. Therefore, in the early years of a 15- or 20-year RV loan, the loan balance is at its highest, meaning the majority of your monthly payment goes toward paying interest. Only a tiny fraction is applied to the principal. It takes many years of payments before the "tipping point" is reached, where more of your monthly payment finally goes toward reducing the actual debt rather than paying the bank's interest.

Can I roll the negative equity from my current RV loan into a brand new camper purchase?

Yes, many RV dealerships will allow you to roll the negative equity from your current upside-down loan into the financing of a brand-new camper, but it is highly risky.

When you do this, the dealer adds your old debt to the purchase price of the new RV. You will instantly be severely underwater on the new RV because you are financing its full retail price, plus its rapid initial depreciation, plus the debt of your old RV. This leads to massive monthly payments and creates a trap that is nearly impossible to escape without defaulting or paying heavily out of pocket.

How do changing market conditions and seasonality impact the real-time trade-in value of an RV?

Real-time RV values are highly volatile and heavily influenced by timing and external economic factors:

- Seasonality: Trade-in values peak in early spring and summer when demand for camping is highest. Values drop significantly in late fall and winter as dealerships avoid paying holding costs for winter storage.

- Economic Factors: High gas prices, rising interest rates, or economic downturns drastically reduce buyer demand, which forces trade-in values to plummet.

- Market Saturation: If manufacturers overproduce or if there is a flood of used RVs hitting the market, the oversupply will depress the trade-in value of your specific camper.

Sources:

Car Subscription vs. Lease / Buy Calculator

Car Subscription vs. Lease / Buy Calculator