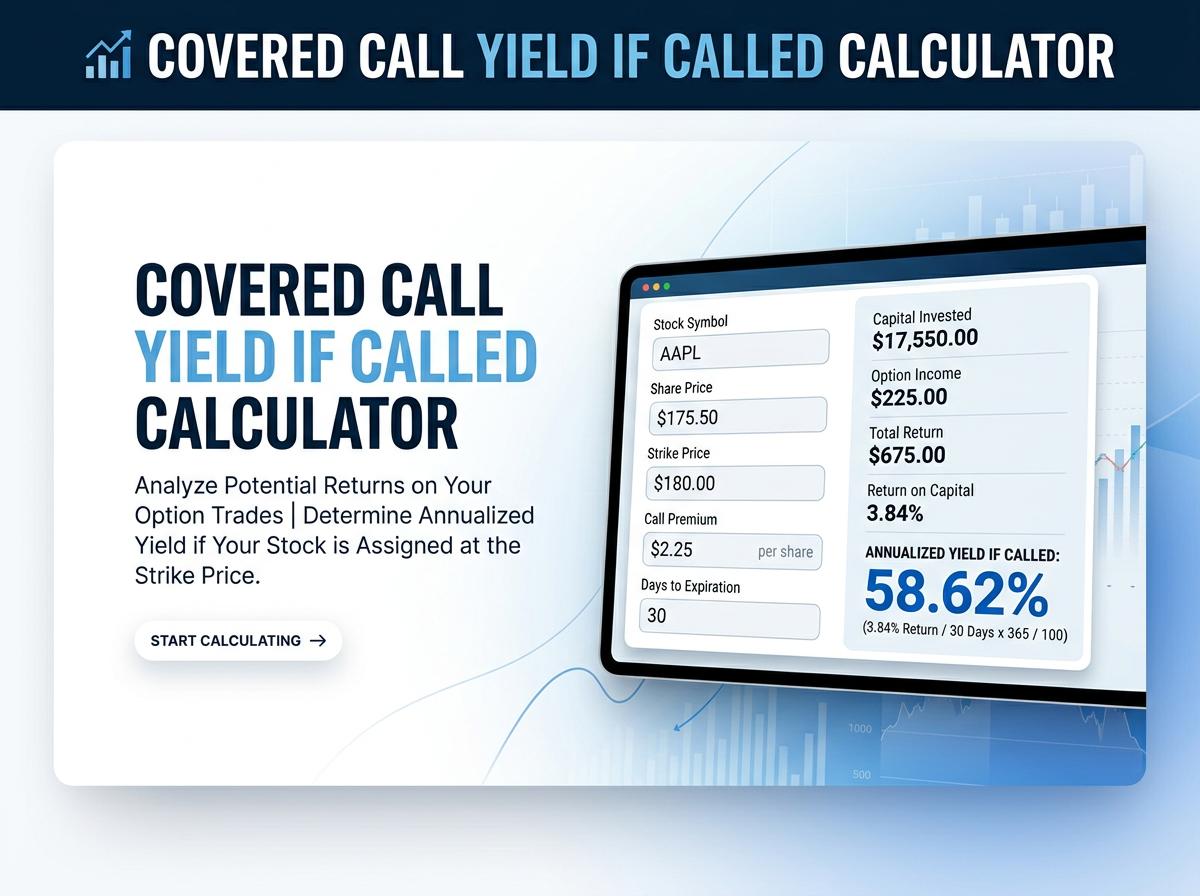

Maximize your options trading profits with our Covered Call Yield if Called Calculator. Instantly compute your total return, annualized yield, and maximum profit potential if your shares are assigned at expiration. Enter your stock price, strike price, and premium to make smarter, data-driven trading decisions today.

Covered Call Yield Calculator

What exactly does yield if called mean in a covered call strategy?

Yield if called is a financial metric representing the total percentage return an investor earns if their underlying stock is assigned (called away) at expiration. This scenario occurs when the stock's market price exceeds the option's predetermined strike price.

The calculation encompasses three main components of profit:

- The premium received upfront from selling the call option.

- Capital appreciation (the positive difference between the stock's purchase price and the strike price).

- Any dividends collected during the holding period.

Ultimately, it illustrates your absolute best-case return for a specific covered call trade, operating under the assumption that the buyer exercises their right to purchase your shares.

How do you calculate the total return if the underlying stock gets assigned?

To calculate the total return if the stock gets assigned, follow these structured steps:

- Determine Capital Gain: Subtract your original purchase price (cost basis) from the option's strike price.

- Add Income: Add the option premium received and any dividends collected before the assignment date.

- Calculate Total Profit: Capital Gain + Premium + Dividends = Total Profit.

- Compute Percentage Return: Divide the Total Profit by your original cost basis (or net investment).

Formula: ((Strike Price - Purchase Price) + Premium + Dividends) / Purchase Price

Multiply the final number by 100 to express it as a percentage.

Does the yield if called represent the absolute maximum profit for the trade?

Yes, the yield if called represents the absolute maximum profit for a standard covered call trade. When you sell a covered call, you contractually agree to sell your shares at the predetermined strike price, regardless of how high the open market price climbs.

Because your upside is strictly capped at that strike price, any stock appreciation beyond that point belongs entirely to the option buyer. Therefore, your total profit is mathematically limited to the combination of the collected option premium, the fixed capital appreciation up to the strike price, and any dividends received prior to assignment.

How do the collected option premium and the strike price dictate this yield?

The collected premium and the chosen strike price are the two primary drivers of your yield if called:

- Option Premium: This provides immediate cash income. A higher premium naturally increases your overall yield and offers a larger cushion against downside risk.

- Strike Price: This dictates your maximum potential capital gain. It sets the exact ceiling at which you are obligated to sell your shares.

These two factors operate on a seesaw. If you choose a higher strike price, you generally receive a lower premium but leave room for higher capital appreciation. Conversely, a lower strike price yields a higher premium upfront but severely limits capital gains, directly shaping your final yield.

What happens to expected dividends if the shares are called away before the ex-dividend date?

If your shares are called away (assigned) before the ex-dividend date, you lose the right to receive the pending dividend. Instead, the option buyer who exercised the contract early and purchased your shares will collect it.

This scenario frequently occurs when a call option is deep in-the-money just before an ex-dividend date—a concept known as dividend risk. Option buyers will rationally exercise early to capture the dividend payout. When calculating your expected yield if called, you must factor in this risk; if early assignment happens, your realized return will exclude that anticipated dividend income.

How do you annualize the yield if called to accurately compare it with other investments?

Annualizing the yield allows you to compare short-term options trades with the yearly returns of other asset classes like bonds or mutual funds. You scale the absolute return based on your specific holding period.

Steps to annualize:

- Calculate the absolute percentage yield if called.

- Count the number of days you held the trade (from execution to expiration or assignment).

- Divide 365 by the number of holding days to find the time factor.

- Multiply the absolute yield by the time factor.

Example: If your absolute yield if called is 4% over a 30-day period, the annualized yield is: 4% × (365 / 30) = 48.6%.

What is the opportunity cost if the underlying stock surges significantly past the strike price?

The opportunity cost in a covered call strategy is the forgone profit that occurs when the stock price surges well beyond your strike price. Because you are contractually obligated to sell your shares at the strike, your capital gains are capped.

For example, if you bought a stock at $50, sold a covered call with a $55 strike, and the stock rockets to $70, you are still forced to sell your shares at $55. The opportunity cost in this scenario is the $15 per share ($70 - $55) that you would have earned had you simply held the stock without writing the call option. This missed upside is the primary trade-off for receiving premium income.

How do out-of-the-money versus in-the-money covered calls change the potential called return?

| Moneyness | Capital Gain Potential | Yield if Called Profile |

|---|---|---|

| Out-of-the-Money (OTM) (Strike > Current Price) |

Positive | Offers a higher total yield if called, as you benefit from both the option premium and the stock's capital appreciation up to the strike price. |

| In-the-Money (ITM) (Strike < Current Price) |

Negative or Zero | Offers a lower yield if called, relying entirely on the extrinsic value of the premium. However, it provides much greater downside protection. |

OTM calls are utilized for growth and income, maximizing potential yield, while ITM calls are more conservative, focusing on downside risk mitigation at the cost of maximum yield.

Do broker commissions and assignment fees significantly reduce your final yield?

Yes, broker commissions and assignment fees can materially reduce your final yield if called, particularly for retail investors trading with small capital amounts or single option contracts.

- Contract Fees: Many brokers charge a per-contract fee (e.g., $0.65) to initially open the position.

- Assignment Fees: Some brokerages charge a flat fee (e.g., $5 to $15) when options are exercised and shares are forcibly called away.

While these fees seem nominal, they cut directly into your net premium. For a small trade yielding a modest $20 profit, a $5 assignment fee destroys 25% of your total return. It is vital to calculate yields net of all broker fees.

What are the specific capital gains tax implications when your shares are called away?

When shares are called away, the tax implications depend heavily on your holding period of the underlying stock and the option's strike price.

- Combined Sale Price: The IRS treats the assignment as a single consolidated transaction. The option premium you received is added to the strike price to determine your total sale proceeds.

- Holding Period: If you held the underlying stock for more than a year before assignment, the gain is taxed at favorable long-term capital gains rates. If held for a year or less, it triggers short-term capital gains (taxed as ordinary income).

Note: Writing a deep in-the-money call can sometimes suspend the holding period of your stock under IRS "straddle" rules, potentially converting expected long-term gains into short-term gains.

Iron Condor Max Loss / Max Profit Calculator

Iron Condor Max Loss / Max Profit Calculator