Calculate the true cost of upfront mutual fund fees with our Front-End Load Impact Calculator. See how sales charges affect your initial investment and long-term returns.

Front-End Load Impact Calculator

What exactly is a front-end load fee in a mutual fund?

A front-end load fee is a one-time sales charge or commission that investors pay when they purchase shares of a mutual fund. This fee is deducted directly from the initial investment amount before the money is actually invested in the fund's assets. The primary purpose of a front-end load is to compensate the financial advisor, broker, or planner who recommended and sold the fund to the investor. Generally, these fees range from 3.75% to 5.75% of the total investment. Because the fee is taken upfront, investors know exactly what they are paying at the time of purchase, rather than dealing with ongoing or back-end sales charges.

How does a front-end load reduce my initial investment capital?

A front-end load reduces your investment capital by deducting the sales charge immediately from your total contribution. Only the remaining balance is used to purchase mutual fund shares. Consequently, less of your money actually goes to work in the market.

| Total Investment | Front-End Load (5%) | Actual Amount Invested |

|---|---|---|

| $10,000 | $500 | $9,500 |

In this example, your starting capital is instantly reduced by $500. Your investment must grow by approximately 5.26% just to return to your original $10,000 outlay.

What is the long-term impact of a front-end load on compound returns?

The long-term impact of a front-end load on compound returns can be significant due to the permanent loss of your initial investing base. Since the fee is deducted upfront, you have fewer shares generating returns over time. Here is how the impact compounds:

- Immediate Capital Loss: A 5% load on $10,000 leaves you with $9,500 invested.

- Missed Growth: The $500 paid as a commission never earns any market returns.

- Compounding Deficit: Over 20 years at an assumed 7% annual return, that missing $500 would have grown to nearly $1,935.

Ultimately, a front-end load stunts your portfolio's growth trajectory because you are compounding a smaller initial sum.

Which mutual fund share classes typically charge a front-end load?

Mutual funds are divided into different share classes, each with its own fee structure. Front-end loads are the defining characteristic of Class A shares.

- Class A Shares: Charge a front-end sales load (usually up to 5.75%) but typically feature lower ongoing annual expenses (12b-1 fees) compared to other classes.

- Class B Shares: Normally charge a back-end load (contingent deferred sales charge) when you sell, not when you buy.

- Class C Shares: Usually have no front-end load but charge higher ongoing annual fees (level-loads).

Because Class A shares have lower ongoing costs, they are generally considered the most cost-effective load option for long-term investors.

How do breakpoints work to reduce the cost of a front-end load?

Breakpoints are essentially volume discounts that mutual funds offer to reduce the front-end sales charge for larger investments. As your investment amount reaches specific thresholds, the percentage of the front-end load decreases.

| Investment Amount | Front-End Load Percentage |

|---|---|

| Less than $50,000 | 5.75% |

| $50,000 - $99,999 | 4.50% |

| $100,000 - $249,999 | 3.50% |

| $1,000,000+ | 0.00% (Waived) |

Investors can achieve breakpoints through a lump-sum purchase, by combining purchases across related accounts (Rights of Accumulation), or by signing a Letter of Intent (LOI) to reach a threshold over 13 months.

Does paying a front-end sales charge guarantee better fund performance?

Absolutely not. Paying a front-end sales charge does not guarantee better mutual fund performance, nor does it mean the fund is managed by superior portfolio managers. The front-end load is strictly a distribution fee meant to compensate the financial professional or brokerage firm for their advice and services in selecting the fund.

Historically, numerous studies have shown that load funds do not outperform no-load funds. In fact, because the front-end load reduces your initial investment capital, a load fund must achieve higher gross returns than a comparable no-load fund just to provide the investor with the same net return over time.

How long does it usually take to break even after paying a front-end load?

The break-even period depends entirely on the size of the front-end load and the fund's market performance. If you pay a typical 5% front-end load, only 95% of your money is actually invested. To get your account balance back to 100% of your original cash outlay, your invested funds must grow by approximately 5.26%.

Assuming an average annualized market return of 7% to 10%, it generally takes roughly 7 to 10 months just to recoup the upfront fee. During a bear market or a period of flat returns, breaking even could take several years, which highlights why load funds are strictly for long-term investors.

What is the difference between a front-end load and a no-load mutual fund?

The primary difference lies in how sales commissions are handled when you purchase the fund:

- Front-End Load Fund: Charges a sales commission immediately upon purchase. If you invest $1,000 with a 5% load, $50 goes to the broker, and only $950 is invested. You are paying for a financial advisor's guidance.

- No-Load Fund: Does not charge any sales commission at purchase. If you invest $1,000, the full $1,000 goes to work in the market immediately. These are usually self-directed investments bought directly from the fund company or via a discount brokerage.

Keep in mind that both types of funds still charge ongoing operating expenses (expense ratios).

How does a front-end load affect the actual net asset value per share I buy?

A front-end load does not change the fund's actual Net Asset Value (NAV), but it does change the price you pay per share. When buying a front-end load fund, you purchase shares at the Public Offering Price (POP).

- NAV (Net Asset Value): The actual underlying value of one share of the mutual fund.

- POP (Public Offering Price): The NAV plus the front-end sales charge.

For example, if the NAV is $10.00 and the load is 5%, the POP is roughly $10.53. You pay $10.53 per share, but your shares are only worth $10.00 the moment you buy them. Consequently, you acquire fewer total shares than if you bought at the NAV.

Can front-end load fees be waived or avoided in certain brokerage accounts?

Yes, front-end loads are frequently waived or entirely avoided under specific circumstances:

- Fee-Based Accounts: If you use an advisor who charges a flat percentage of assets under management (a "wrap" fee), front-end loads for Class A shares are typically waived to avoid double-charging you (Load-Waived Class A shares).

- Employer Retirement Plans: Investments made through institutional 401(k) or 403(b) plans generally waive front-end loads.

- Mutual Fund Supermarkets: Some discount brokerages offer "No Transaction Fee" (NTF) platforms where certain load fees are suppressed.

To avoid them entirely, self-directed investors can simply choose to exclusively purchase no-load mutual funds.

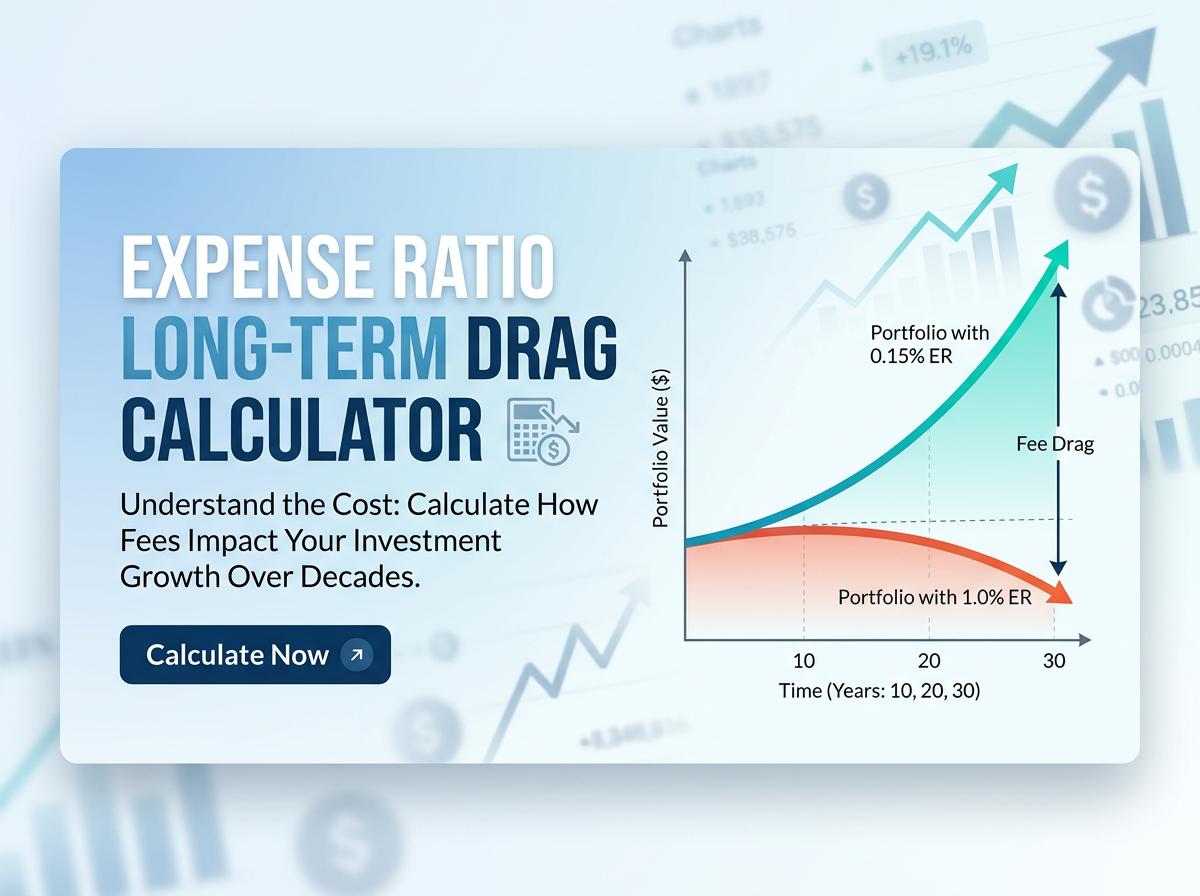

Expense Ratio Long-Term Drag Calculator

Expense Ratio Long-Term Drag Calculator