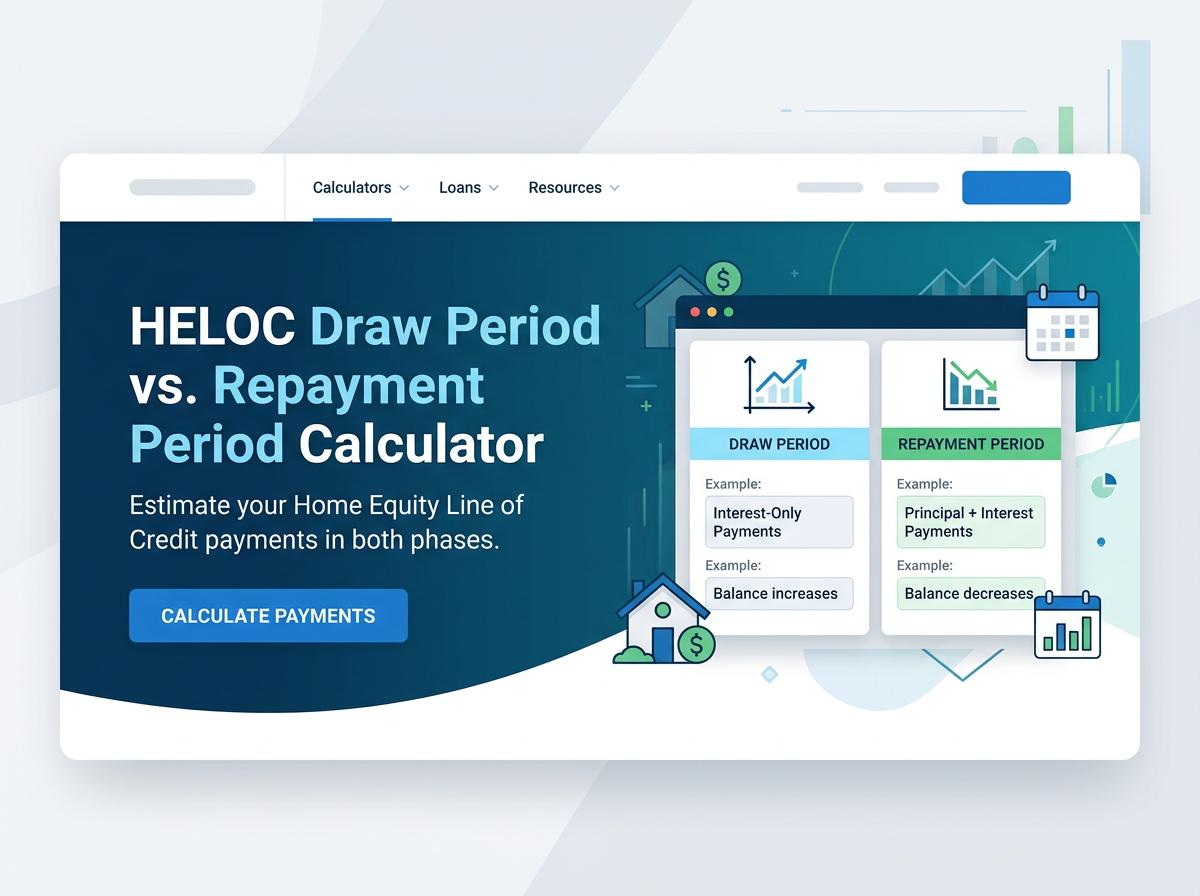

Estimate your HELOC payments with our Draw Period vs. Repayment Period Calculator. Compare interest-only draw phase costs to your future repayment bills to budget smartly and avoid payment shock.

HELOC Calculator

How long do the draw and repayment periods typically last?

A typical Home Equity Line of Credit (HELOC) is divided into two distinct phases, usually totaling a 15- to 30-year lifespan:

| Phase | Typical Duration | Description |

|---|---|---|

| Draw Period | 5 to 10 years | The time you can actively borrow funds using a card or checks. |

| Repayment Period | 10 to 20 years | The time you can no longer borrow and must pay back the principal and interest. |

Can I still borrow money once the repayment period begins?

No, you cannot borrow additional funds once the repayment period begins. During the draw period, a HELOC acts as a revolving line of credit, similar to a credit card. However, the moment the draw period ends and the repayment phase triggers, your credit line is officially frozen.

From that point forward, your sole financial obligation is to pay down the accumulated principal and the associated interest over the remaining term of the loan.

Are minimum payments during the draw period strictly interest-only?

In most cases, minimum payments during the draw period are strictly interest-only, which keeps your initial monthly obligations low. However, this is not a universal rule. Depending on your lender and specific loan agreement, your payments might be structured differently:

- Interest-only: You only pay the monthly interest accrued on the borrowed amount.

- Interest plus principal: Some lenders require a small fraction of the principal to be paid alongside the interest to reduce future payment shock.

How much will my monthly payment increase when repayment starts?

Your monthly payment can increase significantly—often doubling or even tripling—when the repayment period begins. This dramatic payment shock occurs due to two main factors:

- Principal Amortization: You transition from paying only the interest to paying fully amortizing payments that include both interest and principal reduction.

- Variable Rates: If interest rates have risen since you originally opened the HELOC, your new payments will be calculated at that higher rate.

Can I voluntarily pay down the principal during the draw period?

Yes, you can absolutely make voluntary principal payments during the draw period, and financial experts highly recommend doing so. Paying extra provides several major benefits:

- Reduces interest costs: Because interest is calculated on your daily balance, lowering the principal reduces ongoing interest charges.

- Replenishes your credit line: Like a credit card, paying down the principal frees up available credit for future emergencies.

- Prevents payment shock: Reducing your balance early minimizes the drastic payment increase that happens when the repayment period starts.

Is the interest rate fixed or variable during each specific phase?

Traditionally, HELOCs feature a variable interest rate tied to the Prime Rate during both the draw and repayment phases. This means your payment will fluctuate as broader market interest rates change.

However, many modern lenders offer hybrid stability options:

- Fixed-Rate Draw Options: Lenders may allow you to lock in a fixed interest rate on a specific portion of your drawn balance during the draw period.

- Repayment Conversion: Some lenders permit you to convert the entire variable balance to a fixed-rate loan when the repayment period begins.

Will I face a large balloon payment when the draw period ends?

Typically, no. Most standard HELOCs automatically convert into an amortized repayment phase, meaning your balance is paid off gradually through monthly installments over 10 to 20 years.

However, you will face a balloon payment if your specific contract does not include a repayment phase. In these "interest-only with balloon" structures, the entire principal balance becomes due in a single massive lump sum the moment the draw period ends. Always review your loan disclosure to confirm your structure.

How are my monthly payments calculated during the repayment phase?

During the repayment phase, your monthly payment is calculated using a process called amortization. The lender takes your total outstanding principal balance at the end of the draw period and structures it to be paid off completely over the remaining months of the loan.

Each monthly payment is a combination of:

- A portion applied directly to reducing the principal.

- A portion applied to the interest based on the current rate.

Because the rate is generally variable, your payment can still fluctuate during this phase.

Can I refinance or renew the HELOC before the draw period expires?

Yes, refinancing or renewing your HELOC before the draw period expires is a common strategy to avoid the impending payment shock. Your main options include:

- Renewing the HELOC: Opening a new HELOC to pay off the old one, effectively resetting your 10-year interest-only draw period.

- Home Equity Loan: Refinancing the balance into a fixed-rate home equity loan for stable, predictable payments.

- Cash-Out Refinance: Rolling your first mortgage and your HELOC balance into a single, brand-new primary mortgage.

What happens if I cannot afford the higher payments during repayment?

If you cannot afford the higher payments during the repayment phase, you risk defaulting on the loan. Because a HELOC is secured by your property, defaulting could ultimately lead to foreclosure and the loss of your home.

If you anticipate payment issues, take immediate action:

- Contact your lender: Ask about a loan modification or extended repayment term.

- Refinance: Attempt to roll the balance into a lower-interest fixed-rate loan.

- Sell the home: As a last resort, selling allows you to pay off the debt using the proceeds.

Mortgage Recast Amortization Calculator

Mortgage Recast Amortization Calculator