Calculate your eligible Adoption Tax Credit with our free Phasedown Calculator. Enter your Modified Adjusted Gross Income (MAGI) to instantly determine your IRS phase-out reduction and maximize your tax savings.

Adoption Tax Credit Calculator

What is the adoption tax credit phasedown

The adoption tax credit phasedown is a mechanism used by the IRS to gradually reduce the amount of the adoption tax credit available to taxpayers as their income increases. Once a taxpayer's Modified Adjusted Gross Income (MAGI) reaches a specific threshold, the maximum allowable credit begins to decrease incrementally. The credit continues to reduce until the MAGI reaches a higher ceiling, at which point the credit is completely eliminated. This phasedown ensures the financial assistance is primarily targeted toward low- and middle-income families who need support with the high costs of adoption.

How does my income level affect the adoption tax credit

Your income level directly determines how much of the adoption tax credit you are legally eligible to claim:

- Below the phaseout range: You can claim the full amount of your qualified adoption expenses up to the maximum credit limit for that tax year.

- Within the phaseout range: The credit you can claim is gradually reduced (phased down) by a percentage based on how deep your income extends into the phaseout bracket.

- Above the phaseout range: You are completely phased out and not eligible to claim any adoption tax credit.

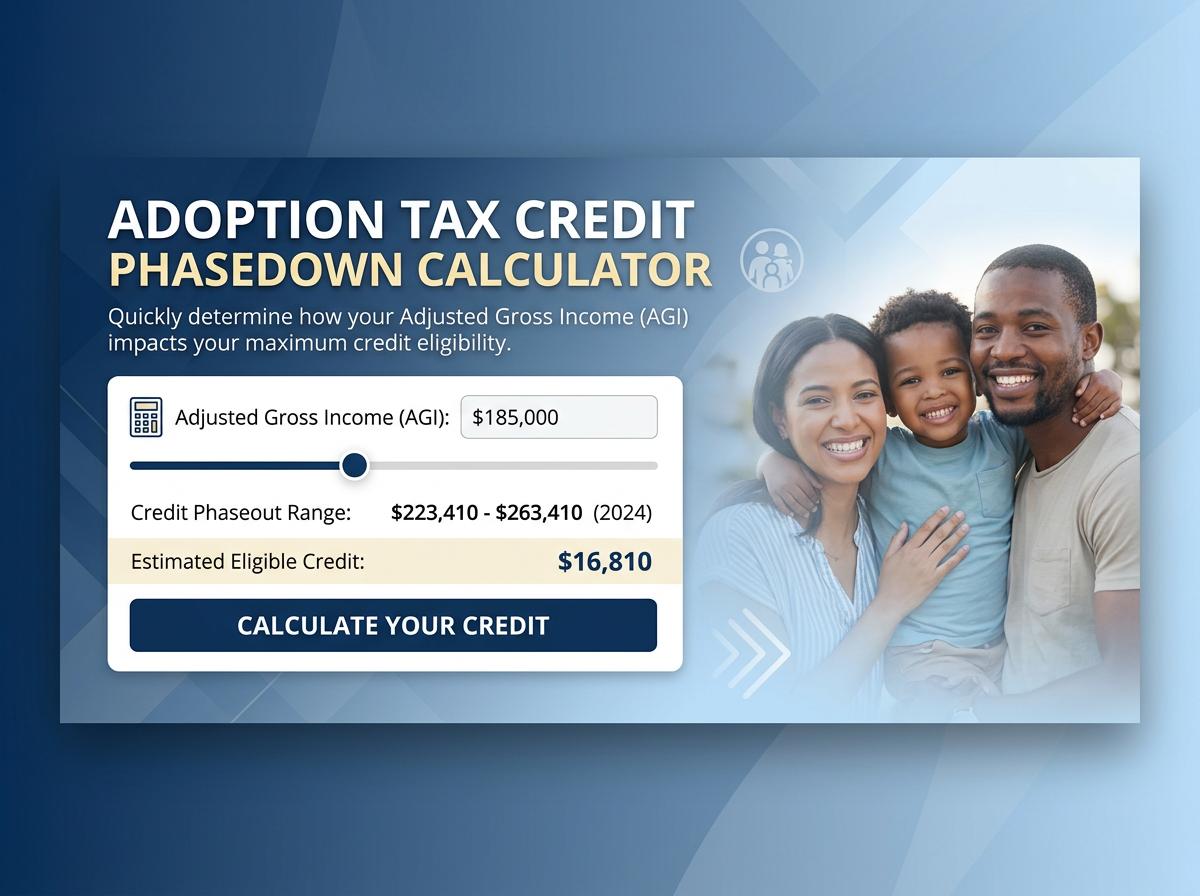

What is the current income phaseout range

The income phaseout range changes annually due to standard inflation adjustments. For the recent tax years, the Modified Adjusted Gross Income (MAGI) phaseout ranges are:

| Tax Year | Phaseout Begins | Phaseout Ends (Credit is $0) |

|---|---|---|

| 2023 | $239,230 | $279,230 |

| 2024 | $252,150 | $292,150 |

How is Modified Adjusted Gross Income calculated for this credit

For the adoption tax credit, your Modified Adjusted Gross Income (MAGI) is calculated by taking your Adjusted Gross Income (AGI) from your standard tax return (Form 1040) and adding back certain tax-free income exclusions. Specifically, you must add back:

- The foreign earned income exclusion

- The foreign housing exclusion or deduction

- Income from Puerto Rico excluded from US tax

- Income from American Samoa excluded from US tax

This recalculated MAGI figure is what the IRS uses to determine your specific phaseout bracket and eligible credit amount.

Does the phasedown apply to special needs adoptions

Yes, the income phasedown rules apply to special needs adoptions exactly as they do to other domestic or international adoptions. Adopting a child with special needs from the U.S. foster care system allows you to claim the maximum adoption tax credit regardless of your actual out-of-pocket expenses. However, your ability to claim this maximum amount is still entirely subject to the MAGI phaseout limits. If your MAGI falls within or above the phaseout range, your special needs adoption credit will be mathematically reduced or completely eliminated.

What happens if my income exceeds the maximum phaseout threshold

If your Modified Adjusted Gross Income (MAGI) exceeds the maximum phaseout threshold for the specific tax year in which you are claiming the credit, the adoption tax credit is completely eliminated. You will not be able to claim any tax credit for your qualified adoption expenses or a special needs adoption, regardless of how much you spent. Furthermore, because no credit is generated, you cannot carry forward any adoption expenses or credits to future tax years.

Can I claim a partial credit if my income falls within the phaseout range

Yes, if your Modified Adjusted Gross Income (MAGI) falls strictly within the upper and lower limits of the phaseout range, you are eligible to claim a partial adoption tax credit. The IRS uses a specific formula to determine your reduction:

- Subtract the lower phaseout limit from your MAGI.

- Divide that result by $40,000 (the standard dollar width of the phaseout window).

- Multiply the resulting percentage by the maximum available credit amount.

- Subtract that figure from the maximum credit to find your allowed partial credit.

Are the phasedown income limits adjusted for inflation every year

Yes, the Internal Revenue Service (IRS) routinely adjusts the adoption tax credit income phasedown limits for inflation every year. Both the threshold where the phaseout begins and the maximum limit where the credit is completely eliminated are updated annually. This adjustment prevents a phenomenon known as "bracket creep," ensuring that taxpayers aren't unfairly penalized or phased out of the credit simply because normal inflation raised their nominal wages. You must use the specific IRS guidelines for your filing year.

How does the phasedown impact my ability to carry forward unused credits

The adoption tax credit is non-refundable, meaning it is limited to your actual tax liability. If your generated credit exceeds your tax liability for the year, you can carry forward the unused portion for up to five subsequent years. However, the phasedown limits the initial amount of credit you are allowed to generate.

If your income triggers a partial phasedown, your total eligible credit is permanently reduced. You can only carry forward the allowed partial credit (minus what you applied in the current year). If you are fully phased out, zero credit is generated, leaving nothing to carry forward.

Which IRS form is used to calculate the specific phasedown amount

To calculate the adoption tax credit and mathematically determine your specific phasedown amount, you must use IRS Form 8839 (Qualified Adoption Expenses).

Part II of this form contains the specific lines required to calculate your MAGI for the purpose of this credit. The form provides step-by-step instructions to subtract the base phaseout threshold from your MAGI, calculate your exact phaseout percentage, and apply that decimal to determine the final, allowable adoption tax credit you can transfer to your Form 1040.

Sources:

Elderly Parent Caregiver Opportunity Cost Calculator

Elderly Parent Caregiver Opportunity Cost Calculator