Use our IVF Financing vs. Multi-Cycle Savings Calculator to compare the true cost of fertility loans versus multi-cycle discount packages. Estimate your monthly payments, uncover hidden fees, and find the smartest financial path for your growing family today.

IVF Financing vs. Multi-Cycle Calculator

What is the total cost difference between loan interest and multi-cycle discounts?

The total cost difference can be substantial. A loan increases your overall expense due to interest rates, while a multi-cycle plan provides a discount but requires high upfront capital.

| Financing Option | Base Cost (2 Cycles) | Additional Costs/Discounts | Estimated Total Cost |

|---|---|---|---|

| Single Cycles + Loan (10% APR) | $24,000 | +$3,800 (Interest over 3 yrs) | $27,800 |

| Multi-Cycle Discount (Cash) | $24,000 | -$4,000 (Package Discount) | $20,000 |

Using a loan means paying a premium over time. Multi-cycle discounts reduce the per-cycle cost, resulting in a potential financial gap of several thousand dollars between the two methods.

Do multi-cycle programs offer a refund if I succeed on the first IVF attempt?

Generally, no. Standard multi-cycle discount programs act as an insurance policy. If you achieve a successful pregnancy on your first IVF attempt, you will not receive a refund for the unused subsequent cycles.

However, there are specialized "Shared Risk" or "Refund" programs. In these specific plans:

- If you succeed on the first try, you pay a premium compared to a single cycle.

- If you exhaust all cycles without taking home a baby, you receive a partial or full refund (often 70% to 100%).

Always review the contract closely, as standard discounted bundles rarely allow prorated refunds for early success.

What credit score is required to qualify for low-interest IVF financing?

To qualify for the most competitive, low-interest IVF financing, lenders typically require a strong credit history. Credit tiers generally break down as follows:

- Excellent (720+): Qualifies for the lowest interest rates (often between 5% and 8% APR) and highest loan amounts.

- Good (680 - 719): Will likely qualify for financing, but with moderate interest rates (9% to 15% APR).

- Fair/Poor (Below 680): May face high interest rates (16% to 30%+ APR), require a co-signer, or be denied altogether.

In addition to credit scores, lenders will heavily evaluate your debt-to-income (DTI) ratio to ensure you can manage the monthly payments alongside existing debts.

Are fertility medications covered under financing loans or multi-cycle packages?

The coverage of fertility medications heavily depends on the payment method you choose:

- Financing Loans: Yes. Personal loans or specialized fertility loans provide cash directly to you or your clinic. You can use these funds to pay for both the IVF procedures and the expensive fertility medications.

- Multi-Cycle Packages: No. Most clinic-based multi-cycle discount programs strictly cover the medical procedures (monitoring, egg retrieval, fertilization, transfer). Medications, which cost $3,000 to $7,000 per cycle, are usually billed separately by third-party pharmacies.

Patients purchasing multi-cycle packages must budget separately for medications or seek pharmaceutical discount programs.

Are there strict age or medical requirements for multi-cycle refund programs?

Yes, clinics impose strict medical and demographic requirements for multi-cycle refund (shared risk) programs to mitigate their financial risk. Common criteria include:

- Age limits: Female patients usually must be under a certain age (often 38 or 39) when using their own eggs. Donor egg programs may have higher limits.

- Ovarian reserve: Normal AMH (Anti-Mullerian Hormone) and FSH levels are required to ensure a reasonable chance of success.

- Medical history: No history of recurrent pregnancy loss, severe male factor infertility, or multiple previously failed IVF cycles.

- BMI: A Body Mass Index (BMI) within the clinic's specified healthy range.

If you do not meet these criteria, you may still qualify for a standard multi-cycle discount, but without the money-back guarantee.

What happens to my financing debt if the IVF treatment is unsuccessful?

If your IVF treatment is unsuccessful, you are still legally obligated to repay the financing debt in full. Fertility financing is typically issued as an unsecured personal loan.

Because the loan is based on your creditworthiness and not tied to the medical outcome, the lender requires regular monthly payments until the principal and interest are completely paid off. This is one of the most significant financial risks of taking out a loan for IVF. You could potentially find yourself paying off thousands of dollars in debt for years after a failed cycle, which can financially hinder alternative family-building options.

Can I use an IVF loan to pay for a multi-cycle savings package?

Yes, absolutely. Many fertility patients combine these two financial strategies. Because multi-cycle savings packages and shared-risk refund programs require a very large upfront payment (often $20,000 to $30,000+), patients frequently secure an IVF loan or a standard personal loan to cover this initial cost.

By doing this, you secure the per-cycle discount or the financial safety net of a refund program from your clinic, while breaking the massive upfront cost into manageable monthly payments through your lender. If you are using a refund program and the cycles fail, the refunded money from the clinic can then be used to pay off the loan balance.

Are there hidden origination fees associated with IVF financing?

Yes, many IVF financing options and personal loans come with origination fees, though they should be clearly disclosed in your loan agreement.

An origination fee is an upfront charge levied by the lender for processing the application. This fee typically ranges from 1% to 8% of the total loan amount. For example, a 5% fee on a $20,000 IVF loan would cost $1,000.

Lenders usually deduct this fee directly from the loan disbursement, meaning you might receive $19,000 despite borrowing $20,000. To accurately compare loans, always look at the Annual Percentage Rate (APR), which factors in both the interest rate and the origination fees.

Which option provides better financial protection against multiple failed cycles?

A multi-cycle refund program (shared risk program) provides vastly superior financial protection against multiple failed cycles compared to financing.

With an IVF loan, you assume 100% of the financial risk. If the cycles fail, you are left empty-handed but still burdened with years of debt payments.

Conversely, a shared risk program shifts the financial burden back to the clinic. If you exhaust all cycles included in your package without achieving a live birth, the clinic refunds a significant portion (usually 70% to 100%) of your initial payment. This financial safety net allows you to use those refunded funds for other family-building avenues.

Is there a financial penalty for canceling a multi-cycle plan before completion?

Yes, usually there is a financial penalty. If you voluntarily withdraw from a multi-cycle discount program before using all your cycles—and without achieving a successful pregnancy—the clinic will recalculate the services you've already received.

Typically, they will convert the completed cycles from the discounted package rate back to the clinic's higher, standard single-cycle rate. They will subtract this higher cost, along with administrative or cancellation fees, from your initial upfront deposit.

As a result, you may receive a much smaller refund than anticipated. It is crucial to review the cancellation policy in your clinic's financial contract before committing.

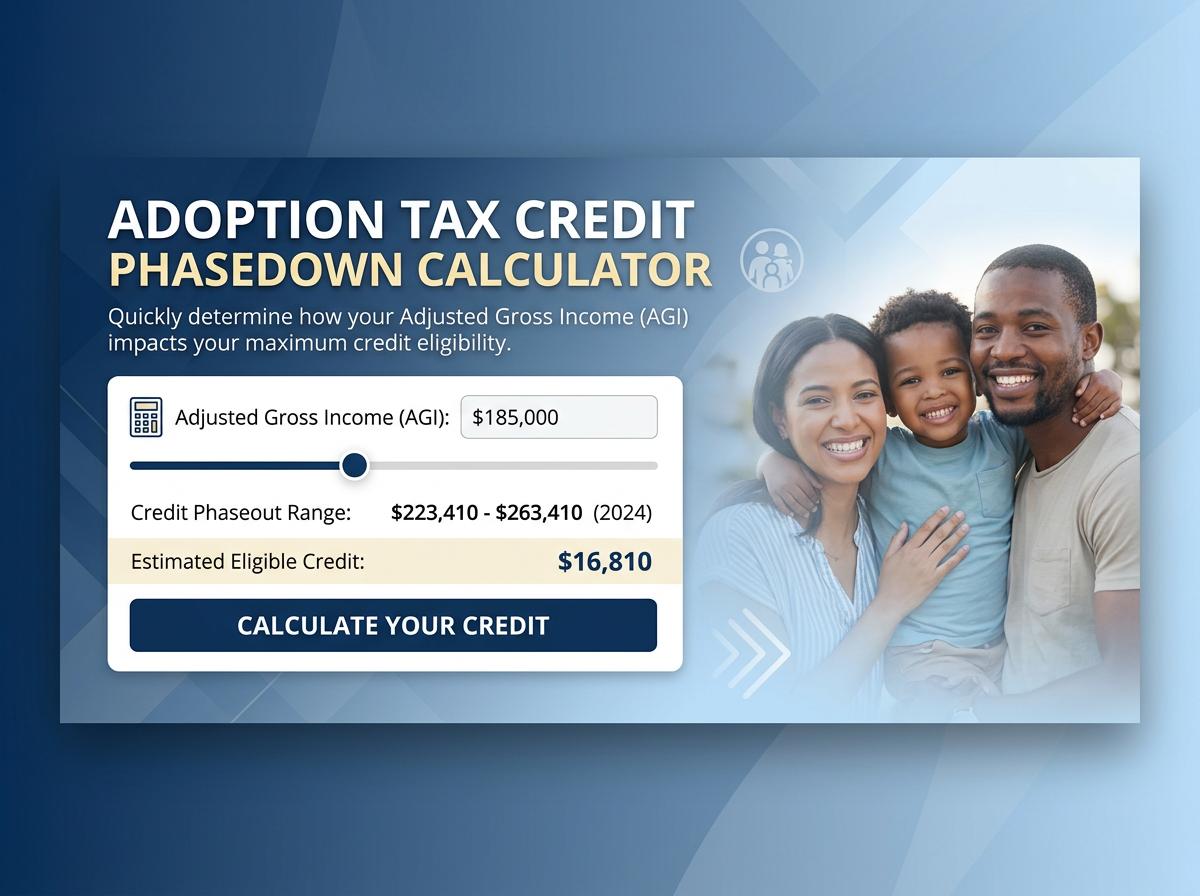

Adoption Tax Credit Phasedown Calculator

Adoption Tax Credit Phasedown Calculator