Discover the true cost of short-term borrowing with our free Payday Loan APR Equivalency Calculator. Quickly convert flat fees and short repayment terms into an Annual Percentage Rate (APR) to compare loan options, uncover hidden costs, and make smarter, more informed financial decisions.

Payday Loan APR Calculator

What is payday loan APR equivalency

Payday loan APR equivalency is the mathematical conversion of a short-term loan's flat fee into an Annual Percentage Rate (APR). Since payday loans are typically repaid within 14 to 30 days, their costs are often expressed as a simple fixed fee (e.g., $15 per $100 borrowed).

However, the Truth in Lending Act requires lenders to express loan costs as an APR to allow consumers to compare them fairly against other credit products, like credit cards or personal loans. The equivalency shows what the interest rate would effectively be if that exact fee structure was stretched and compounded over a full 365-day year.

How do you calculate the annualized rate of a short-term payday loan

To calculate the annualized rate (APR) of a short-term payday loan, you follow a straightforward mathematical formula to project the short-term cost over a full year:

- Divide the finance charge (the flat fee) by the loan amount.

- Multiply the result by 365 (the number of days in a year).

- Divide that number by the term of the loan in days (e.g., 14 days).

- Multiply the final figure by 100 to convert it into a percentage.

Formula: APR = (Fee / Loan Amount) x (365 / Loan Term) x 100

What is the typical APR for a standard two-week payday loan

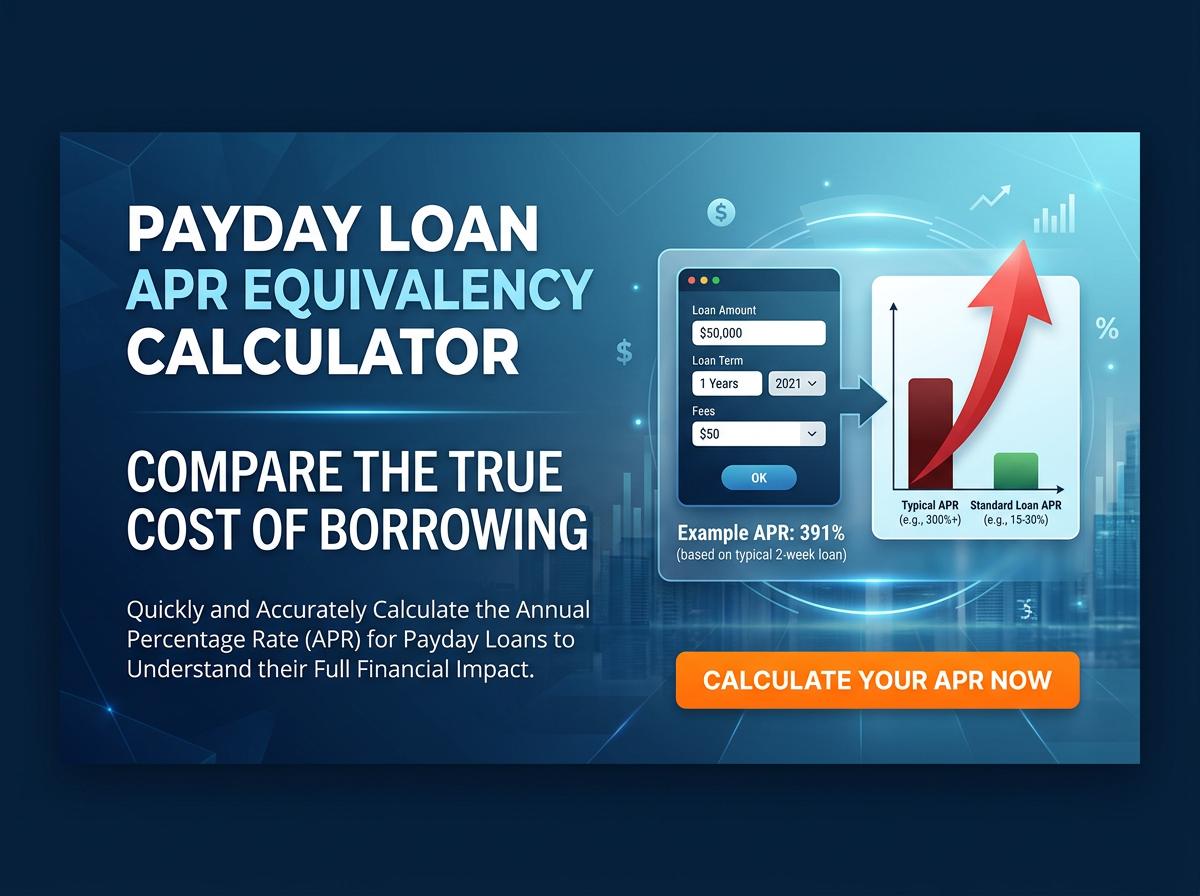

The typical APR for a standard two-week payday loan ranges between 391% and 521%. This exorbitant rate stems from the standard fee structure utilized by most payday lenders across the United States.

| Loan Term | Fee per $100 Borrowed | Equivalent APR |

|---|---|---|

| 14 Days | $15 | 391.07% |

| 14 Days | $20 | 521.43% |

How does a flat fee convert into an annual percentage rate

A flat fee converts into an annual percentage rate (APR) by projecting the short-term cost over a full 365-day year. Because an APR measures the cost of borrowing for an entire year, the flat fee must be multiplied by the number of loan cycles that fit into one year.

If a loan lasts 14 days, there are roughly 26 loan cycles in a single year (365 ÷ 14 = 26.07). You then multiply the flat fee percentage by 26 to find the APR. Therefore, a seemingly small 15% flat fee over two weeks compounds exponentially into an annualized rate of nearly 400%.

What does a fifteen dollar fee per hundred dollars borrowed equal in APR

A $15 fee per $100 borrowed for a standard 14-day term equals an APR of exactly 391%. Here is the step-by-step breakdown of how that equates:

- Fee percentage: $15 / $100 = 0.15 (or 15%)

- Daily interest rate: 0.15 / 14 days = 0.01071 (or 1.071% per day)

- Annualized rate: 0.01071 x 365 days = 3.9107

- Percentage conversion: 3.9107 x 100 = 391.07%

It is important to note that if the loan term changes, the APR shifts. For a 30-day term, that exact same $15 fee equals an APR of roughly 182%.

Why do payday loans have drastically higher APRs than credit cards

Payday loans have drastically higher APRs than credit cards primarily due to their ultra-short repayment timelines and high-risk lending environments.

- Short Duration: Credit card APRs calculate interest over an entire year, whereas payday fees are applied over just two weeks. Annualizing a two-week fee exponentially inflates the percentage.

- High Risk: Payday lenders typically cater to subprime borrowers with poor credit histories and require no collateral, significantly increasing the statistical risk of default.

- Operating Costs: Processing numerous small-dollar loans incurs high administrative and physical retail overhead relative to the tiny loan sizes.

Why do payday lenders prefer advertising flat fees instead of the APR

Payday lenders heavily prefer advertising flat fees because they appear far less intimidating and much more manageable to borrowers than a massive APR. Stating "just $15 per $100 borrowed" sounds like a small, affordable convenience fee.

In contrast, advertising a "391% APR" highlights the extreme cost of the credit and could easily scare off potential customers. Furthermore, lenders argue that since the loan is intended to be paid back in two weeks, an annualized rate is an inaccurate representation of the borrower's actual out-of-pocket cost, making the flat fee a more "practical" marketing tool.

How does rolling over a payday loan affect the true compounded cost

Rolling over a payday loan drastically increases the true compounded cost, often trapping the borrower in a devastating cycle of debt. When a borrower rolls over a loan, they pay a brand new flat fee simply to extend the due date, without reducing the original principal balance at all.

For example, rolling over a $300 loan (with a $45 fee) three times means paying $135 in fees alone, while still owing the original $300 principal. This continuous cycle turns a one-time short-term fee into a recurring financial drain, resulting in effective APRs that can surge well beyond 600%.

Why is understanding APR equivalency crucial for borrowers

Understanding APR equivalency is crucial because it creates a universal, standardized metric that allows borrowers to make "apples-to-apples" comparisons between vastly different credit products.

Without knowing the APR, it is incredibly difficult to compare a $15 flat fee on a two-week payday loan against an 18% annual interest rate on a standard credit card. By converting everything into an annual percentage rate, borrowers instantly see that the payday loan's 391% APR is extraordinarily expensive. This vital transparency empowers consumers to seek cheaper borrowing options and avoid high-cost debt traps.

How does a payday loan APR compare to a standard personal loan rate

A payday loan APR is astronomically higher than a standard personal loan rate. While a typical personal loan is designed for longer terms (years) and assesses interest gradually, payday loans pack high fees into a tiny two-week window.

| Loan Type | Typical APR Range | Repayment Term |

|---|---|---|

| Payday Loan | 391% - 600% | 14 to 30 Days |

| Personal Loan (Good Credit) | 6% - 15% | 1 to 5 Years |

| Personal Loan (Bad Credit) | 18% - 36% | 1 to 5 Years |

Even the most expensive subprime personal loans legally cap at around 36% APR, making standard payday loans roughly ten to twenty times more expensive.

Collections Settlement Pay-for-Delete Calculator

Collections Settlement Pay-for-Delete Calculator