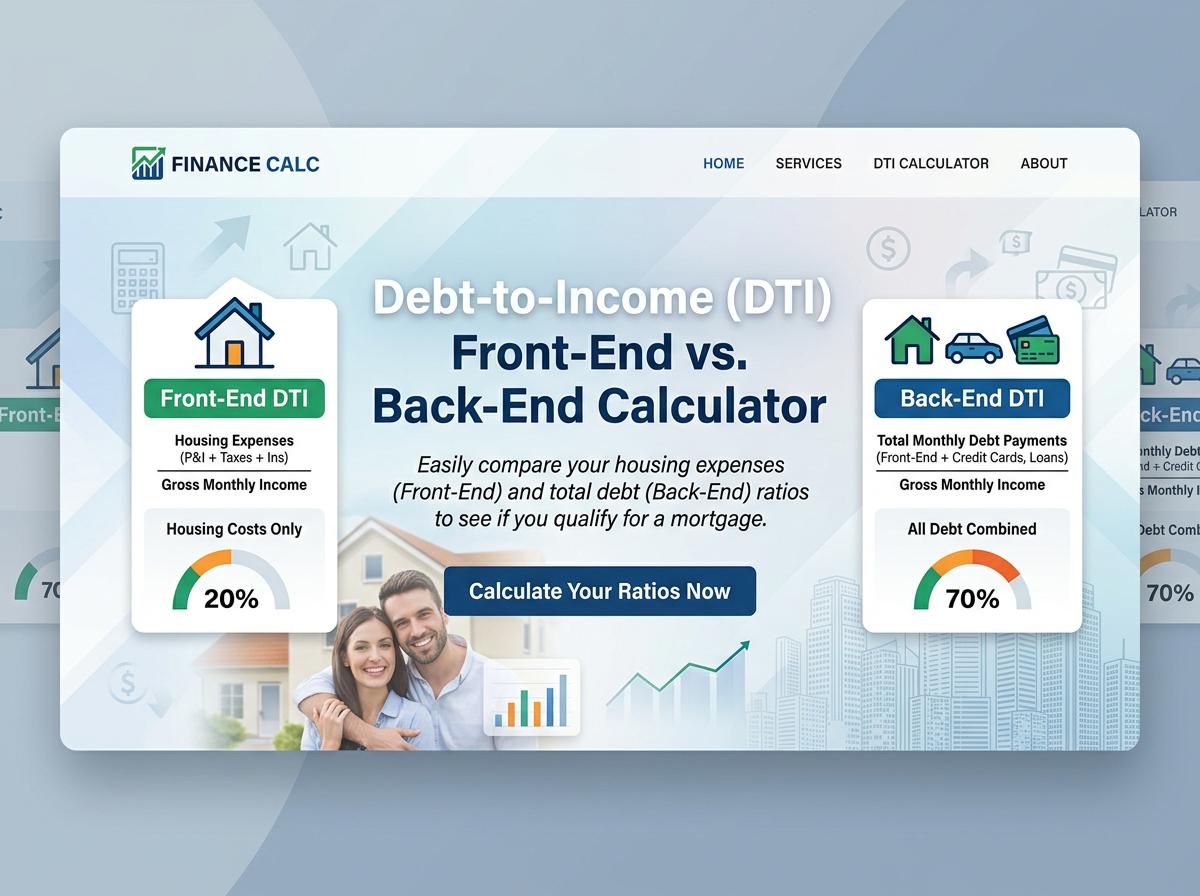

Calculate your front-end and back-end debt-to-income (DTI) ratios instantly. Use our free DTI calculator to compare your housing expenses and total monthly debts against your gross income. Discover your mortgage approval odds and take control of your homebuying readiness today!

DTI Calculator

What is the exact difference between front-end and back-end DTI?

The exact difference lies in the scope of debts measured against your gross monthly income:

- Front-end DTI: Also known as the housing ratio, it only measures your anticipated monthly housing expenses (mortgage principal, interest, taxes, and insurance) against your income.

- Back-end DTI: This measures all of your recurring monthly debt obligations—including the anticipated housing costs plus credit cards, auto loans, and other debts—against your income.

Essentially, the front-end evaluates housing affordability, while the back-end evaluates total financial solvency.

How do you calculate a front-end debt-to-income ratio?

To calculate your front-end DTI, follow these specific steps:

- Determine total housing costs: Add up your projected monthly mortgage payment (Principal and Interest), property taxes, homeowner's insurance, and HOA fees (commonly known as PITI).

- Determine gross income: Calculate your total gross monthly income (your earnings before taxes and deductions).

- Divide: Divide the total housing costs by your gross monthly income.

- Convert to percentage: Multiply the result by 100.

Formula: (Total Monthly Housing Costs / Gross Monthly Income) x 100 = Front-End DTI%

Which specific expenses are included in the back-end DTI calculation?

The back-end DTI incorporates your total housing payment plus all other recurring monthly debt obligations. Specific expenses included are:

- Proposed monthly housing payment (PITI + HOA)

- Minimum monthly credit card payments

- Auto loan or lease payments

- Student loan payments

- Personal loan payments

- Mandatory child support or alimony payments

- Other legal, recurring debt obligations

Note: General living expenses like groceries, utility bills, health insurance, and cell phone bills are not included in this calculation.

Why do mortgage lenders evaluate both DTI ratios instead of just one?

Mortgage lenders evaluate both ratios to get a comprehensive view of a borrower's financial risk profile.

If a lender only looked at the front-end DTI, they might approve a borrower whose income easily covers the mortgage, but fail to realize the borrower is drowning in credit card and student loan debt. Conversely, looking only at the back-end DTI might obscure the fact that an uncomfortably large portion of the borrower's income is tied strictly to a single housing payment.

Using both ensures the borrower can comfortably afford the home and maintain their existing financial obligations without defaulting.

What is considered an ideal front-end DTI percentage for a homebuyer?

For most traditional mortgage lenders, the ideal front-end DTI percentage is 28% or lower. This standard is often referred to as the first half of the traditional "28/36 rule" in mortgage lending.

| Front-End DTI | Lender View |

|---|---|

| Under 28% | Ideal / Excellent |

| 28% - 31% | Acceptable (common limit for FHA loans) |

| Over 31% | Risky (requires compensating factors) |

Keeping your front-end DTI at or below 28% shows lenders that you will not be "house poor" and have income left over for daily living expenses.

What is the maximum back-end DTI typically allowed for conventional loans?

Traditionally, the standard maximum back-end DTI for a conventional loan is 36%. However, modern lending standards have become significantly more flexible.

Today, many conventional lenders will allow a maximum back-end DTI of up to 43%. In certain cases, lenders may push the maximum limit to 45% or even 50% if the borrower possesses strong "compensating factors." These factors include an exceptionally high credit score, a large down payment, or substantial cash reserves.

Despite this flexibility, anything above 43% typically triggers stricter automated underwriting scrutiny.

Does the front-end DTI calculation include auto loans or credit card minimums?

No, the front-end DTI calculation does not include auto loans, credit card minimums, or any other consumer debt.

The front-end DTI is strictly isolated to housing-related expenses. It only factors in your prospective mortgage principal, interest, property taxes, homeowner's insurance, and any homeowners association (HOA) fees. All of your other recurring debt obligations are reserved exclusively for the back-end DTI calculation.

How does your gross monthly income impact both of these calculations?

Your gross monthly income (your total earnings before taxes and deductions) serves as the mathematical foundation—the denominator—for both calculations.

- Higher Gross Income: A higher income directly lowers both DTI ratios, making you appear less risky to lenders and qualifying you for larger loan amounts.

- Lower Gross Income: A lower income raises both DTI percentages, meaning your debt consumes a larger slice of your earnings, which limits borrowing power.

Because gross income is used rather than net (take-home) pay, borrowers must remember that their actual available cash is less than the calculations suggest.

Which of the two DTI ratios is generally deemed more critical by lenders?

The back-end DTI ratio is universally deemed more critical by mortgage lenders.

While the front-end ratio shows housing affordability, the back-end ratio provides a complete, holistic picture of a borrower's financial health. It encompasses all mandatory debt obligations, giving lenders a precise metric of how close a borrower is to financial insolvency.

In fact, many modern loan programs (such as certain Fannie Mae or Freddie Mac guidelines) have eliminated strict front-end DTI requirements entirely, focusing solely on the back-end limit to determine final loan approval.

How can you effectively lower your back-end DTI before applying for a mortgage?

If your back-end DTI is too high, you can lower it by adjusting either your debt or your income before applying:

- Aggressively pay down debt: Focus on eliminating smaller installment loans or paying off credit card balances entirely to remove those minimum payments from your monthly liability sheet.

- Increase your gross income: Pick up extra shifts, start a documented side hustle, or ask for a raise. Ensure this income is consistent and provable so lenders will count it.

- Avoid new credit: Do not finance a new car, take out personal loans, or open new credit cards prior to getting a mortgage.

Sources:

Credit Score Simulator by Action Calculator

Credit Score Simulator by Action Calculator