Optimize your retirement strategy with our Target Date Fund Glidepath Exposure Calculator. Easily visualize how your portfolio's asset allocation shifts between equities and fixed income over time. Analyze risk exposure, compare funds, and ensure your investment glidepath aligns with your long-term retirement goals.

Glidepath Exposure Calculator

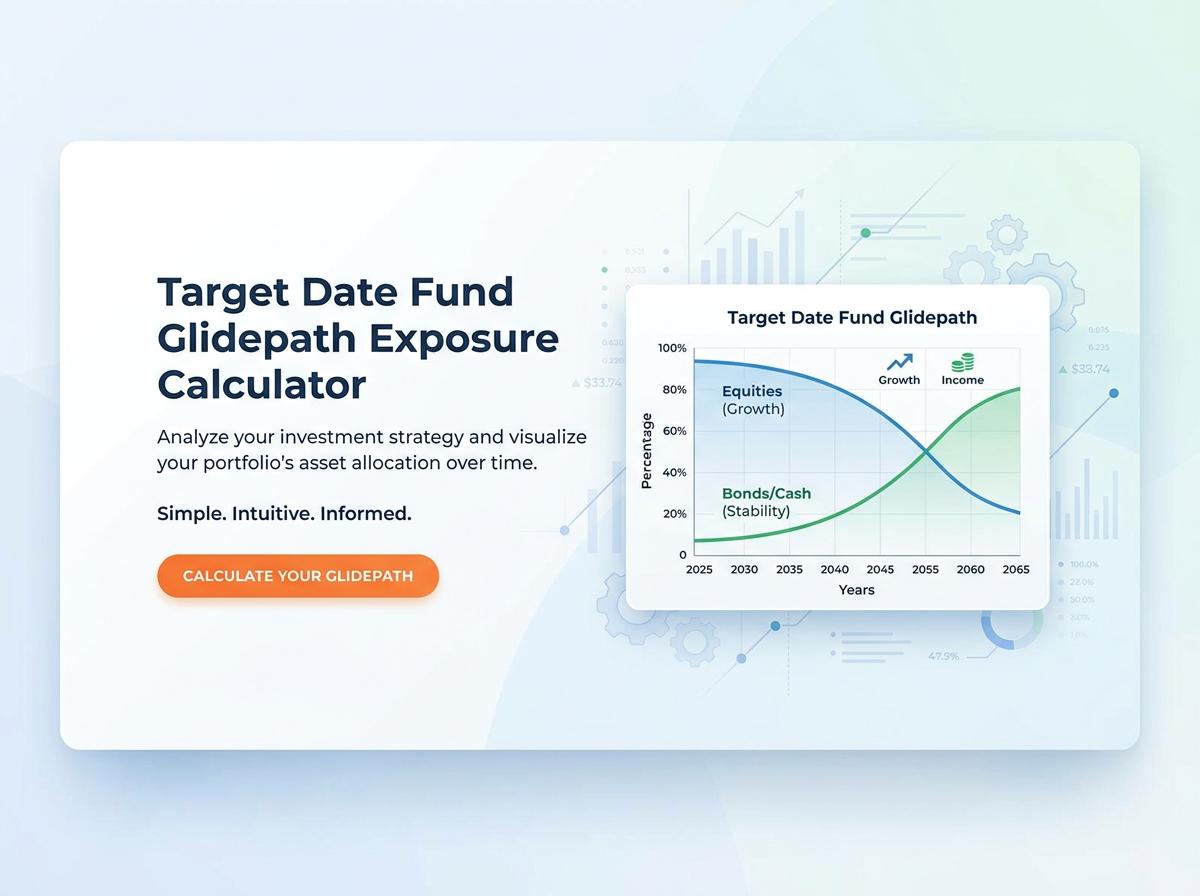

What is the starting equity allocation?

The starting equity allocation in a Target Date Fund (TDF) represents the maximum stock exposure given to young investors farthest from their retirement date. Industry standards typically set this initial allocation heavily toward growth.

- Standard Range: Typically between 90% and 95% equity.

- Purpose: This aggressive early posture maximizes long-term capital growth.

Because young investors have a 30- to 40-year time horizon, they are best positioned to recover from short-term market volatility, making a high starting equity allocation the standard across major fund providers like Vanguard and Fidelity.

Does the glidepath manage to or through retirement?

Glidepaths are broadly categorized into two distinct management philosophies regarding the target retirement date:

| Type | Description |

|---|---|

| "To" Retirement | The equity allocation reaches its most conservative point exactly at the target date. It assumes the investor might cash out or move to a stable income fund upon retiring. |

| "Through" Retirement | The equity allocation continues to gradually decrease for 10 to 15 years after the target date. It assumes the investor stays in the fund throughout retirement. |

Most major modern TDFs use a "Through" approach to combat the risk of an investor outliving their assets.

What is the final landing point allocation?

The final landing point allocation is the ultimate, static asset mix a glidepath reaches when it stops becoming more conservative. This occurs either at the target date or 10-15 years post-retirement.

- "To" Funds: Often land at roughly 30% to 40% equity at the retirement date.

- "Through" Funds: Typically land at a more conservative 20% to 30% equity, but reach this final point later in the investor's life.

At the landing point, the primary focus of the portfolio shifts entirely from capital appreciation to capital preservation and steady income generation.

Which specific asset classes are included?

Target Date Funds are highly diversified. A typical fund includes a broad mix of the following asset classes:

- Equities (Stocks)

- Domestic Large-Cap, Mid-Cap, and Small-Cap

- International Developed Markets

- Emerging Markets

- Fixed Income (Bonds)

- U.S. Investment Grade Bonds

- Treasury Inflation-Protected Securities (TIPS)

- High-Yield (Junk) Bonds and International Bonds

- Cash & Equivalents

- Money Market Funds

- Short-term Treasury Bills

The exact asset mix depends on the specific fund provider and the current stage of the glidepath.

How steep is the equity drop near the target date?

The steepness of the equity drop—often called the roll-down rate—varies significantly among fund families. It dictates how rapidly the portfolio shifts from riskier stocks to safer bonds in the years immediately preceding and following the target retirement date.

Generally, the roll-down accelerates roughly 10 years before the target date. For example, a fund might drop from 75% equity to 50% equity over a 10-year span (averaging a 2.5% drop per year).

Steeper drops minimize sequence-of-returns risk just before retirement but can limit late-stage portfolio growth. Funds managing "to" retirement typically feature a much steeper drop right before the target date compared to "through" funds.

Are the underlying investment funds active or passive?

Target date funds can be constructed using active funds, passive (index) funds, or a blend of both:

| Strategy | Characteristics |

|---|---|

| Passive | Utilizes underlying index funds. These offer the lowest expense ratios, high tax efficiency, and transparent market returns. |

| Active | Employs portfolio managers attempting to outperform the market through security selection. These carry higher management fees. |

| Blend | Combines both, often using passive funds for efficient markets (e.g., U.S. Large Cap) and active managers for less efficient areas (e.g., Emerging Markets). |

Does the exposure include alternative investments?

Historically, most conventional TDFs have avoided alternative investments due to higher fees, liquidity constraints, and structural complexity. However, modern institutional glidepaths are increasingly incorporating limited alternative exposure to enhance diversification.

When alternatives are included, they typically consist of:

- Real Estate Investment Trusts (REITs): Utilized for income generation and inflation protection.

- Commodities: Used as a hedge against broader market inflation.

- Liquid Alternatives: Such as absolute return or market-neutral strategies.

This exposure is usually capped at a small percentage (e.g., 2% to 10% of the total portfolio) and is far more common in actively managed funds than in pure index-based TDFs.

How does the fund balance inflation and longevity risks?

TDFs face a delicate balancing act between outliving one's money (longevity risk) and losing purchasing power (inflation risk). They manage this balance by adjusting allocations across the timeline:

- Combating Longevity Risk:

- Maintaining high equity exposure (90%+) during the early accumulation phase.

- Using a "through" glidepath to retain 30-50% equity exposure well into retirement for continued growth.

- Combating Inflation Risk:

- Gradually introducing Treasury Inflation-Protected Securities (TIPS) as the target date approaches.

- Allocating portions to real assets like REITs and commodities.

- Keeping a base level of equities, which historically outpace inflation.

Do the fees change as the asset allocation shifts?

Whether fees change over time depends entirely on the pricing structure chosen by the Target Date Fund provider:

- Acquired Fund Fees (Bottom-Up Pricing): The total expense ratio is the weighted average of the underlying funds. Under this model, fees generally decrease as the glidepath shifts away from expensive equity/international funds and into cheaper fixed-income and cash funds.

- Unified/Level Pricing: Many modern providers charge a single, fixed top-level fee that covers all management costs. Under this unified structure, the expense ratio remains completely static, regardless of how the underlying asset allocation shifts as the investor ages.

Can managers tactically deviate from the set glidepath?

The ability of managers to deviate from the published glidepath depends on the fund's specific mandate:

| Approach | Manager Flexibility |

|---|---|

| Strictly Strategic | Managers must adhere tightly to the predefined glidepath. Rebalancing is mechanical, with no room for market timing. Most passive TDFs use this approach. |

| Tactical Asset Allocation | Managers are granted a "tactical band" (typically ±5% to ±10%). This allows them to overweight or underweight specific asset classes temporarily based on macroeconomic forecasts. |

Tactical deviations aim to capture extra returns or protect against imminent downturns, though this introduces active manager risk.

Sources:

401(k) Company Match Vesting Schedule Calculator

401(k) Company Match Vesting Schedule Calculator